How to Make Your Child a Millionaire

Learn how to turn just €62/month into a million for your child using smart investments, government subsidies, and tax strategies to make your child a millionaire! 💰👶

Key Takeaways

- You can make your child a millionaire with €62/month, using government subsidies and investments.

- Raising kids is costly, but government subsidies help reduce the financial burden significantly.

- Mutterschaftsgeld ensures salary continuation during maternity leave; Elterngeld supports raising children in early years.

- Avoid savings accounts, insurance plans, and Bausparvertrag due to poor returns; better investment options exist for growth.

- Invest in ETFs, real estate, and precious metals to ensure long-term growth, stability, and financial security for your child’s future.

- Start early, invest smartly, and help secure a prosperous financial future for your child.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationIntroduction

Raising children is an expensive journey, but there’s a powerful way to give them a financial head start in life. By strategically investing a modest €62 per month, you can make your child a millionaire by the time they retire.

This method leverages government subsidies, tax savings, and compound interest to secure a prosperous future for your child. In this article, we’ll walk through step-by-step how you can achieve this without needing to be a financial expert.

The High Cost of Raising Children in Germany

Raising a child in Germany is costly. According to the German Statistical Office, the average child costs around €763 per month, amounting to a staggering €165,000 by the time they reach adulthood. This figure is based on 2018 data, and considering rising living costs, it’s likely much higher today.

Thankfully, German parents have access to numerous government subsidies to help ease the financial burden. From Mutterschaftsgeld to Kindergeld, these subsidies can also be strategically invested to provide long-term benefits for your child’s financial future.

Government Benefits You Can Take Advantage Of

Several government benefits are available to help parents in Germany manage the costs of raising children. First is Mutterschaftsgeld, which covers the maternity leave period—6 weeks before and 8 weeks after birth. This benefit, combined with your employer’s contribution, ensures your net salary stays intact.

Next, Elterngeld supports parents who take time off work to care for their newborn, and Kindergeld provides at least €250 per month until your child turns 18 or even up to age 25. Parents can also claim Kinderfreibetrag, a tax-free allowance, which can sometimes be more beneficial than receiving Kindergeld. These funds and tax deductions can be used to jumpstart your child’s future by investing wisely.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe Power of Compounding Interest

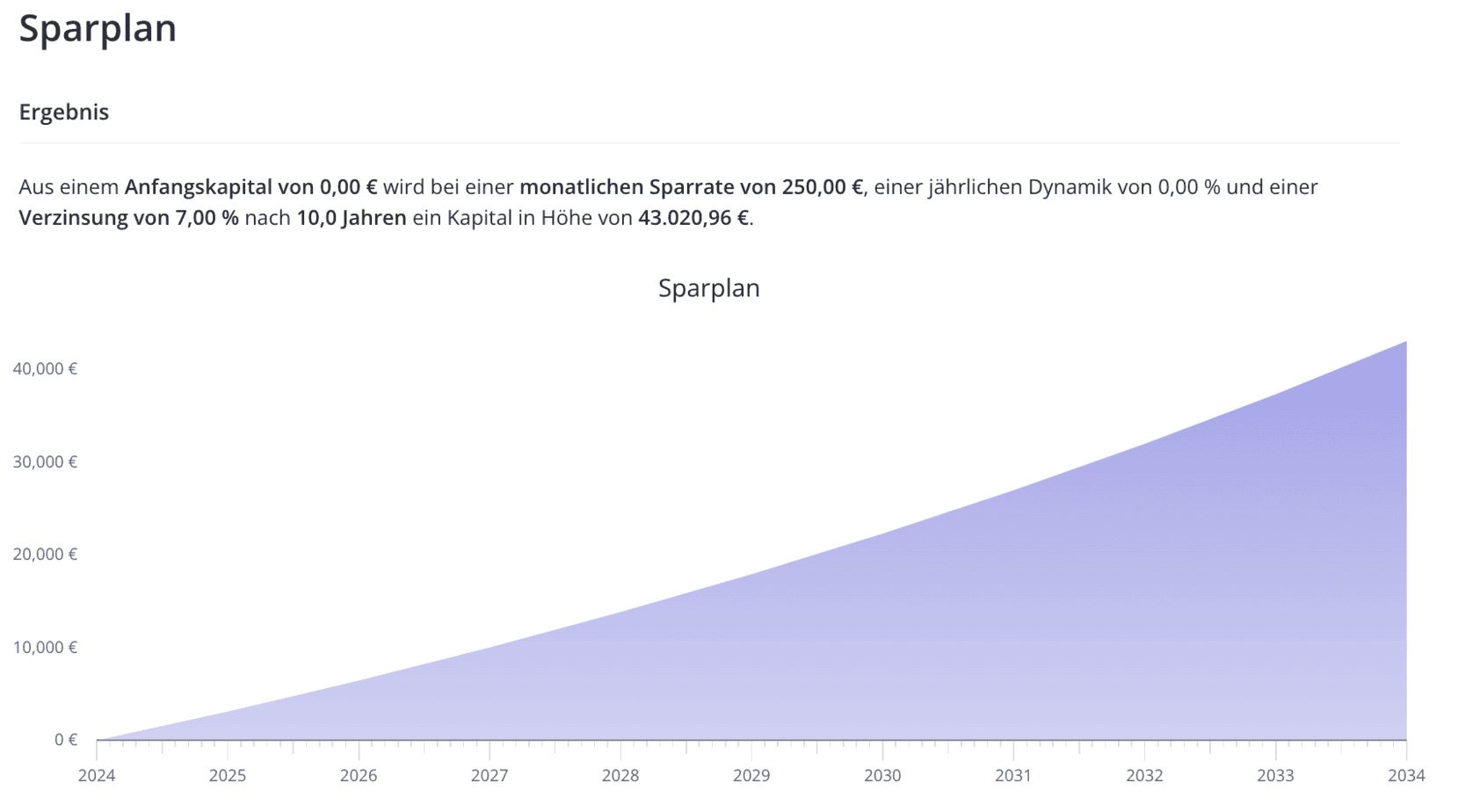

Compounding interest is one of the most powerful tools for growing wealth, especially when you start early. If you invest the €250 Kindergeld every month for your child, it could grow to €43,000 in just 10 years.

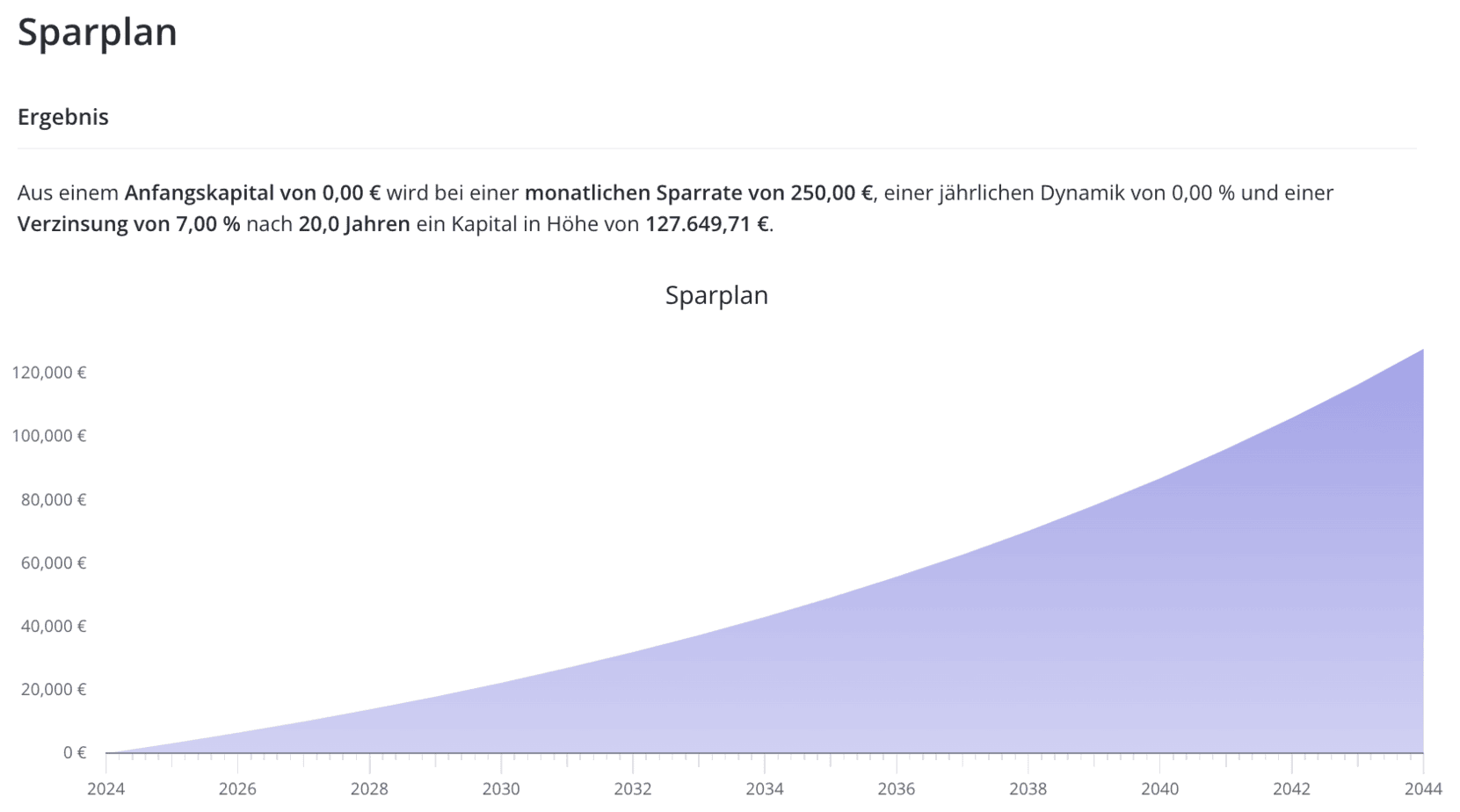

If you keep the investment going for 20 years, it could increase to almost €130,000. Imagine your child having such a large sum to use for their first home or other life investments.

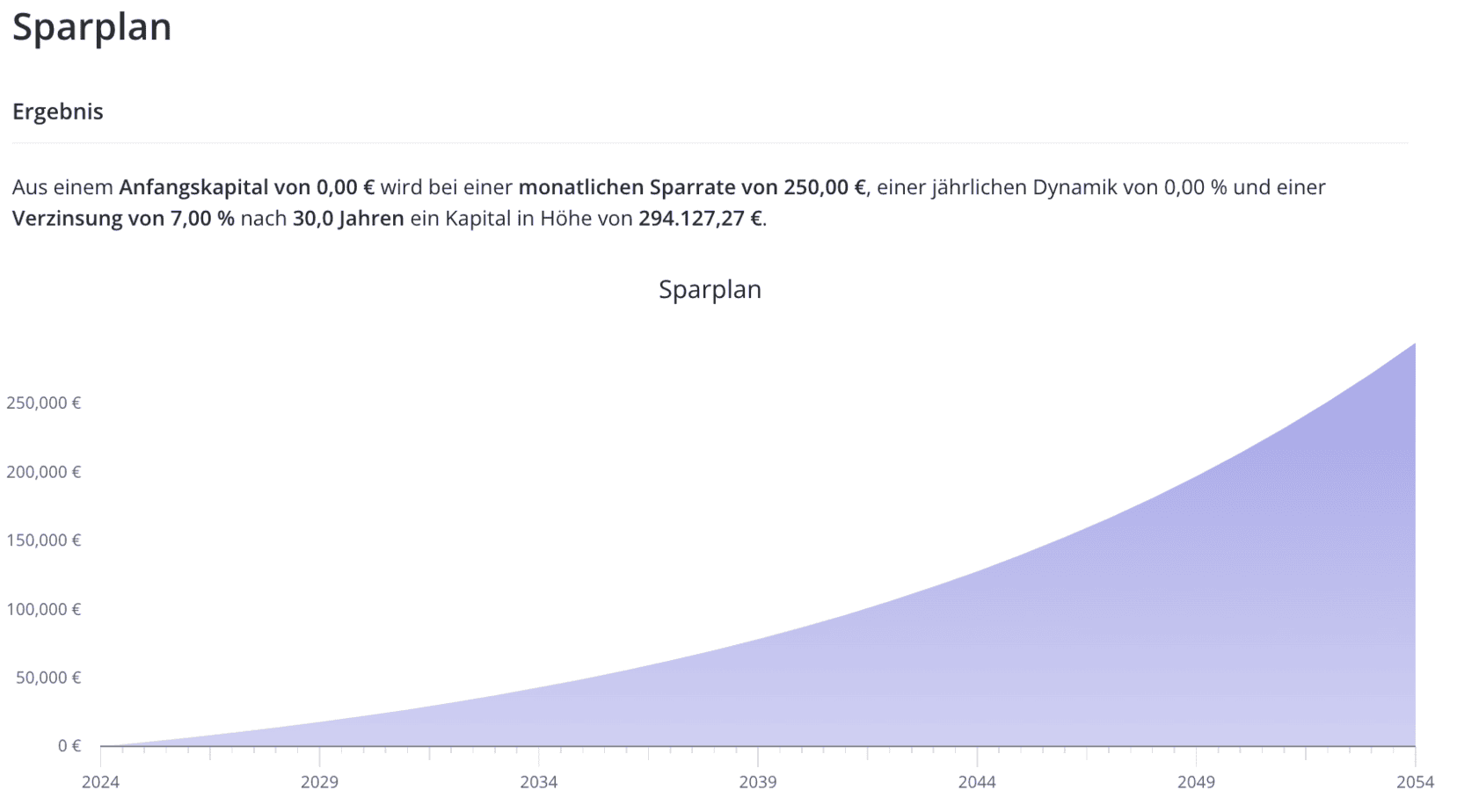

Keep it going for 30 years, and you’re looking at nearly €300,000! The earlier you start, the more time compound interest has to work its magic, turning even small contributions into significant wealth.

Investing Wisely: What to Avoid

Savings Accounts:

While investing is crucial, it’s just as important to know what to avoid. Many German parents still rely on outdated investment methods like savings accounts, which offer little to no interest. The current interest rates mean your money is essentially just sitting there, doing nothing.

This mindset stems from past experiences like the Telekom stock crash in the 90s, which left many Germans wary of riskier investments. However, when it comes to long-term growth, avoiding savings accounts and exploring better options is key to maximizing returns for your child’s future.

Why You Should Avoid Kid-Specific Insurance Plans

Germany offers various insurance plans designed for children, but they often don’t make financial sense. These insurance products, such as Ausbildungsversicherung, combine savings with insurance policies like disability insurance. However, the returns are notoriously low—often as little as 1.25%.

When even a standard savings account can yield better returns, it’s clear that these insurance plans are a poor investment choice. Instead, stick with higher-return options like Kidspolice, ETFs, or real estate to secure your child’s financial future.

The Pitfalls of Bausparvertrag

Another common investment mistake is the Bausparvertrag, which promises home-buying benefits but rarely delivers. With even lower returns than kid-specific insurance plans and rigid mortgage payback terms, the Bausparvertrag is often a dead-end for your money. It’s a tool that doesn’t fit modern financial needs, and you should avoid it at all costs.

Instead, if real estate is your goal, consider purchasing a property directly. You can buy a small property and pay off the mortgage while your child is still young. By the time they’re adults, you can gift or inherit the property tax-free, giving them a valuable asset to start their life with.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationInvesting Wisely: What to Get

ETFs: The Modern Investment Solution

ETFs (Exchange Traded Funds) are among the best investment options for growing wealth. These funds are essentially baskets of various stocks or bonds that you can easily buy through a brokerage or a kidspolice. They offer diversity, simplicity, and solid returns.

Investing in ETFs for your child provides long-term growth potential while minimizing risk. One important tip: setting up a brokerage account in your child’s name allows them to benefit from tax-free capital gains of up to €1,000 annually.

However, there are tax implications and potential drawbacks, like your child gaining control of the account at 18. For more control and tax efficiency, consider putting ETFs into a “pension” account, where funds grow tax-free until you decide to release them.

Real Estate: A Smart Long-Term Investment

Real estate can be one of the smartest investments you make for your child’s future. Buying a small property and paying off the mortgage while your child grows up means they can start adulthood with a paid-off home and passive rental income.

This strategy provides financial stability and opens doors to future opportunities. Plus, as long as the property is valued at less than €400,000, you can gift it to your child completely tax-free. It’s an investment that grows in value and offers long-term security.

The Case for Gold and Precious Metals

Precious metals like gold and silver are often overlooked, but they can be a solid addition to a well-rounded investment portfolio. Over the past five years, gold has seen an impressive performance, growing by more than 70%.

While past performance doesn’t guarantee future results, gold has historically been a stable investment. One major advantage of investing in gold is the ability to avoid the 25% tax on profits if you hold it for at least a year. This makes it an attractive option for those looking to diversify their child’s portfolio and hedge against market volatility.

Conclusion

Investing for your child is not just about setting aside money—it’s about building a strong financial foundation for their future. With just €62 per month and the right investment strategies, you can potentially turn that modest sum into a million euros by the time your child retires, so that you can make your child a millionaire.

The combination of government subsidies, tax savings, and smart investing will not only secure their financial future but also teach them valuable money habits. Start early, invest wisely, and your child will thank you for setting them up for life-long financial success. To book a free meeting with us, use this link.

Pingback: How to Become a Millionaire in Germany on an Average Salary