The Hidden Costs of Neobrokers in Germany: There's No Free Lunch in Investing

"Free" investing isn't free. We expose the hidden costs of Neobrokers in Germany that you're paying without even knowing it. 💰

Key Takeaways

- Neobrokers aren’t truly “free“; they profit from hidden costs that erode your returns, which the EU plans to ban.

- A hidden cost in every trade, the bid-ask spread is often significantly inflated by Neobrokers.

- Neobrokers profit by routing your trades to market makers, creating a conflict of interest against you.

- Neobrokers receive “thank you” payments from ETF providers, which you ultimately pay in fees.

- A hidden German tax on accumulating ETFs can cost you money even if your investments decline.

- Neobrokers bake currency conversion fees into the exchange rate, eating your profits.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe "Free" Investing Trap: What You Need to Know About Neobrokers

€1, 99 cents, free, free, free. Neobrokers like Scalable Capital or Trade Republic promise you “free” investing, yet they manage to make MILLIONS from your trades. We all naturally love getting things for free; it feels like an immediate win. But these companies have hundreds of employees, expensive offices, and complex IT systems to run. So how can they possibly operate for free?

Here’s the simple truth: they aren’t free. And guess who is ultimately paying the bill? You are. They generate revenue straight from your account in ways that are deliberately designed to be invisible to the average investor. This is precisely why the EU wants to ban their core business model as early as 2026. This legislation aims to increase transparency and fairness for individual investors.

We’re here to break down these hidden costs that quietly eat your returns. Because in the world of investing, a fundamental rule holds true: there’s no such thing as a free lunch. Understanding these hidden charges is the first step toward making smarter, more informed decisions with your money.

The Bid-Ask Spread: The Inconvenient Truth of Every Trade

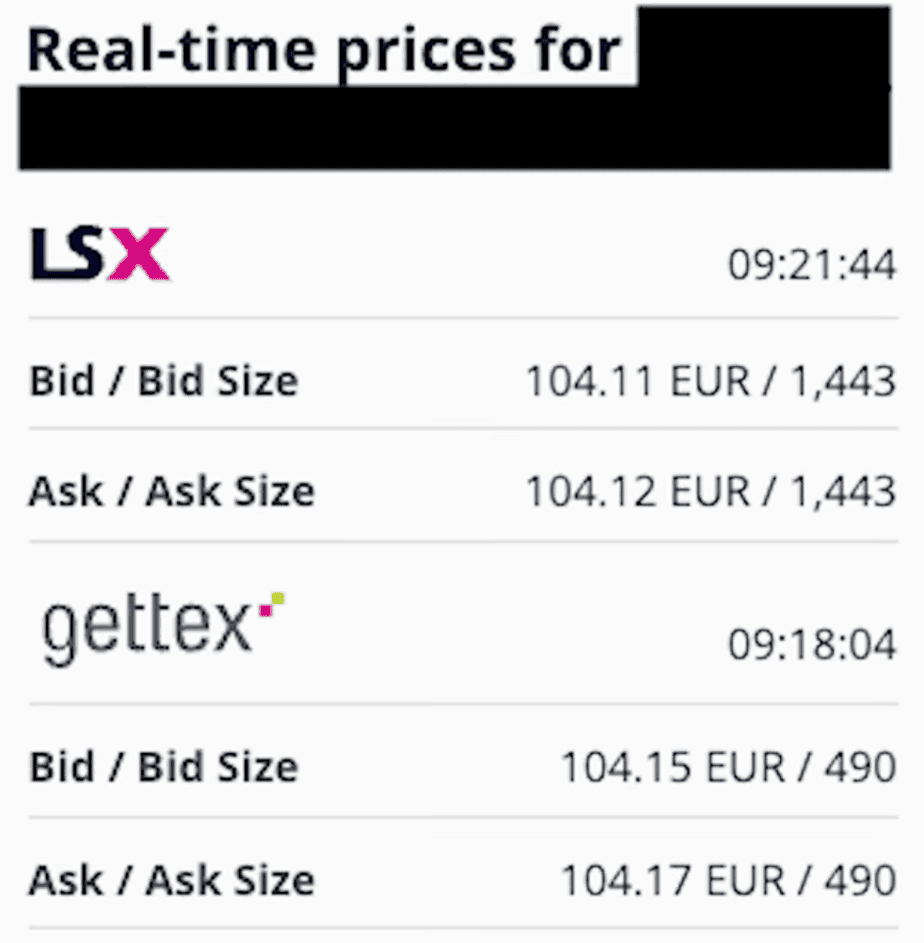

Let’s start with the very first hidden cost you encounter in investing—the so-called bid-ask spread. While it sounds technical, the concept is actually pretty simple. Almost every investment, whether it’s shares, ETFs, or even precious metals like gold, has two prices, not just one. Think of it like an auction: the bid (the lower price) is what a buyer is willing to pay, while the ask (the higher price) is what a seller wants. The difference between these two prices is the spread—the built-in cost of trading. This is why, the very moment you buy a share or an ETF, you’re already a little bit in the red. You bought at the higher ask price, but you could only sell it back to the market at the lower bid price.

In traditional markets, this spread is often minuscule. For example, you might see an ETF on a standard exchange with a 104.12€ ask and a 104.11€ bid, just a 1-cent spread. But here’s where it gets interesting—and a little uncomfortable—with Neobrokers. Neobrokers like Scalable Capital or Trade Republic may not charge you a visible commission, but they still profit from the price you trade at. This is because they don’t just connect you to the market; they decide which market you get. This is thanks to a practice called Payment for Order Flow, which we’ll discuss in a moment. Since a spread of a few cents doesn’t make much money, they often widen it. While the normal spread for a specific trade should be a mere 3 cents, a neobroker might charge you a spread of 4.38 cents. That’s a staggering 14,500% higher than it should be, and that cost comes straight out of your pocket, invisibly eating your returns.

The good news is you can reduce the damage, even with a Neobroker. Trade European shares during peak hours (9:00 to 17:30) when activity is highest and spreads are tightest. For U.S. stocks, trade in the afternoon when Wall Street is open. Most importantly, use limit orders instead of market orders. That way, you control the maximum you’ll pay or the minimum you’ll accept. Just remember: the trade might not go through if the market moves away from your specified price.

Payment for Order Flow (PFOF): The Conflict of Interest

Earlier, we mentioned that your Neobroker decides which market you get. Remember that? This practice is known as Payment for Order Flow (PFOF). When you place a trade, Neobrokers often don’t send it to the exchange that would give you the best possible price or the smallest spread. Instead, they route your order to a so-called market maker—a company that is always ready to buy or sell a specific security.

The market maker earns money from the spread and then shares a portion of that profit with your broker. This is precisely what the EU plans to ban in 2026, following the lead of several other countries, including the U.S., which have already taken steps to curb this practice. The reason for the ban is simple: it creates a fundamental conflict of interest. Your broker and the market maker both want to make money from your trade. And with a tiny 1-cent spread, there’s barely anything to earn. That’s why market makers can subtly nudge the spread in their favor, meaning you end up with a worse price than you might get on a transparent public exchange.

For them, it’s not just about executing your trade; it’s about monetizing it. You can limit the damage by trading during peak hours, using limit orders, and comparing execution prices across different brokers. But as long as PFOF exists, the incentives are stacked against you, which is exactly why regulators want it gone.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationETF Kickbacks & Commissions: The "Thank You" You Don't See

But Payment for Order Flow is not the only side income for Neobrokers. They can also receive kickbacks or commissions from third parties, which are often market makers or ETF providers. Here’s how this works: when you buy an ETF, the provider might pay your broker a “thank you” fee for bringing you in as an investor. And since that payment ultimately comes from the ETF’s total expense ratio—the fees you pay to hold the fund—it’s ultimately your money.

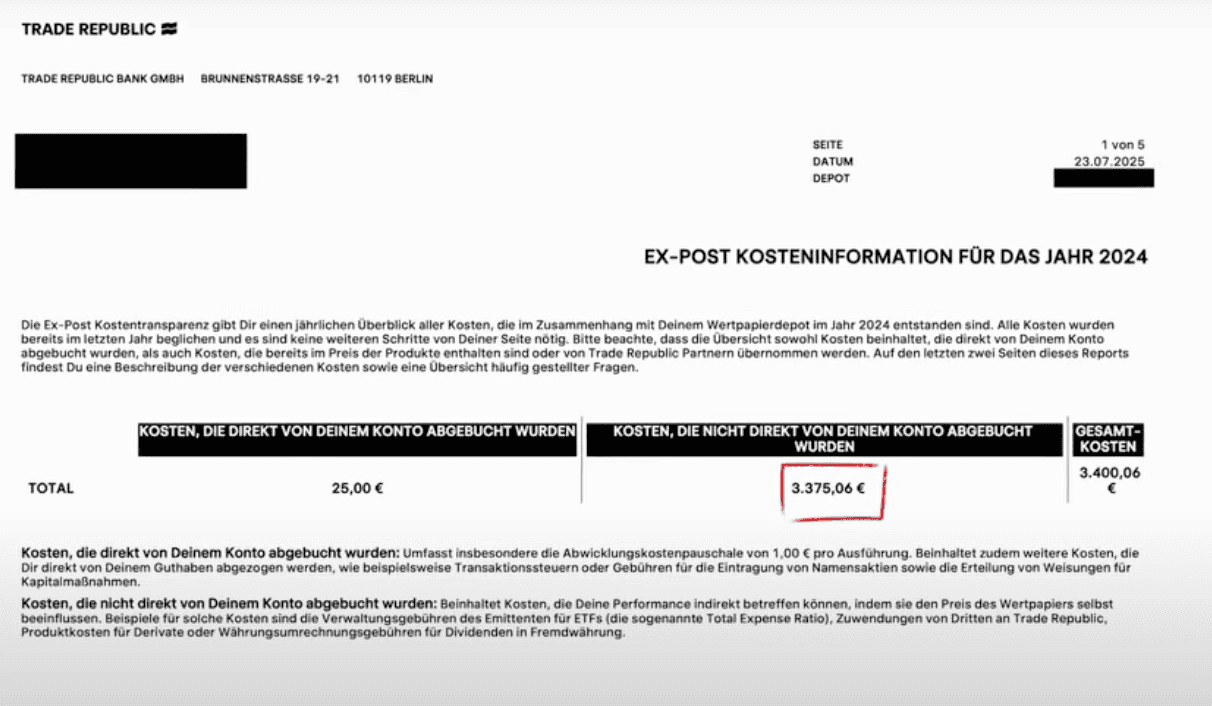

These kickbacks rarely appear in your Neobroker’s app or on your regular statements. To see the real picture, you have to dig into the obscure and often complex ex-post cost information documents that are legally required to be provided. One of our clients actually sent us his numbers for 2024. Trade Republic claimed he paid only €25 in trading fees. But when we meticulously checked his ex-post statement, the total was a shocking €3,375. That’s an astonishing 13,400% more than he thought he was paying. And with a total trading volume of just €11,500, nearly 30% of his investments went straight to fees. That’s simply insane.

The danger is obvious: you might think you’re picking the best investment for your portfolio when you’re really picking the one that’s best for your broker because it offers them a larger kickback. Our advice is to always compare similar products, especially ETFs, and never just blindly choose the first ones that appear in your broker’s search results. And if you want personal, unbiased help choosing the right investments for your financial goals, you can book a free meeting.

The Vorabpauschale Tax: A "Cost" for Every German Investor

The next hidden “cost” is a uniquely German issue that hits every investor in the country, even if you’ve never used a Neobroker. What if we told you there’s a tax that can hit you even if your investments go down in value? It sounds completely crazy, right? But in Germany, that’s exactly what can happen, and it’s called the Vorabpauschale (Advanced Lump Sum Tax). If you own a distributing ETF, the tax office (Finanzamt) takes its cut every time you receive a dividend, which is fair enough. But with accumulating ETFs, they might otherwise have to wait years, or even decades, to collect taxes on your gains.

Well, not anymore. If you hold an accumulating ETF in a regular brokerage account, the Finanzamt will calculate your ETF’s return each year and tax you on a portion of it. This applies even if you haven’t sold a single share and the gain is only on paper. The most infuriating part is this: if you paid tax on these fictional profits this year and the market crashes next year, you do not get any of your taxes back. If you want to learn how to avoid the Vorabpauschale and discover 9 other common ETF mistakes that could cost you thousands of Euros, read the linked article. Because whether it’s hidden costs or hidden taxes, they all eat your returns, so you can’t afford to ignore them if you invest in Germany.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationForeign Exchange (Forex) Fees: The Invisible Currency Tax

Have you ever bought a U.S. stock or something from your home country and thought, “Great, I only paid the share price”? What if we told you your broker might have charged you another fee without ever calling it a fee? That’s what happens with foreign exchange (forex) fees. Every time you buy or sell in a currency different from your account’s base currency—like buying a U.S. stock in a Euro account—your broker has to convert the money. The trick is that neobrokers rarely show this as a separate charge. Instead, they cleverly bake it into the exchange rate.

The official market rate might be one thing, but you get a slightly worse rate. And that hidden difference goes straight into your broker’s pocket. For example, if you buy €10,000 worth of U.S. stocks with a 0.25% markup, €25 is gone, instantly. And for other, less-traded currencies, the markup can be 0.5% or more. If you trade often or receive foreign dividends, these little cuts add up fast and significantly erode your returns over time.

To reduce the damage, our advice is to trade in your account’s base currency whenever possible—so Euros for most of you. Choose brokers with a reputation for low forex markups. And always check the actual conversion rate before you click ‘buy.’ Sometimes, the real cost of a trade isn’t in the stock itself; it’s in the currency exchange. Remember: investing is not just about making money; it’s about keeping it. Thanks for reading—and bis zum nächsten Mal!

Pingback: From Broke to €100,000: Your Complete Financial Guide for Germany