German Payslip Explained 2026: Why your Netto changed

Understand why your "Netto" changed this month. From the €12,348 tax-free allowance to the new €77,400 PKV threshold, we explain the 2026 German payroll shifts in plain English. 💸

Key Takeaways

- The 2026 tax-free allowance provides relief, but rising social security caps and health surcharges often negate these gains.

- Verify your tax class and church tax status to avoid losing hundreds of Euros to avoidable default settings.

- “Geldwerter Vorteil” like JobTickets adds taxable value to your gross, which can slightly lower your final net take-home pay.

- High earners pay up to 3.5x more tax than average earners due to Germany’s steep progressive tax system.

- Social security deductions stop at certain income limits, offering a “maximum price” advantage for those earning six figures.

- High earners above €77,400 can switch to private health insurance, often securing better coverage for lower monthly costs.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationWhy You Can Earn 100.000€ and Still Feel Poor in Germany

February is the first month where you see the REAL impact of the new 2026 payroll updates on your bank account. Germany has raised the basic tax-free allowance (Grundfreibetrag) to €12,348—a welcome change that protects more of your income from taxes than ever before. However, at the same time, contributions for health insurance and public pensions have climbed as well, primarily due to higher income caps and an increased average additional contribution (Zusatzbeitrag) of 2.9%.

This creates a frustrating “tug-of-war” on your payslip: the government gives with one hand through tax relief while the social security system takes with the other. So the question remains: is your payslip working for you, or are you simply a passenger in a system designed to keep you from building wealth? Let’s decode every single line of your 2026 payslip to ensure you aren’t leaving money on the table.

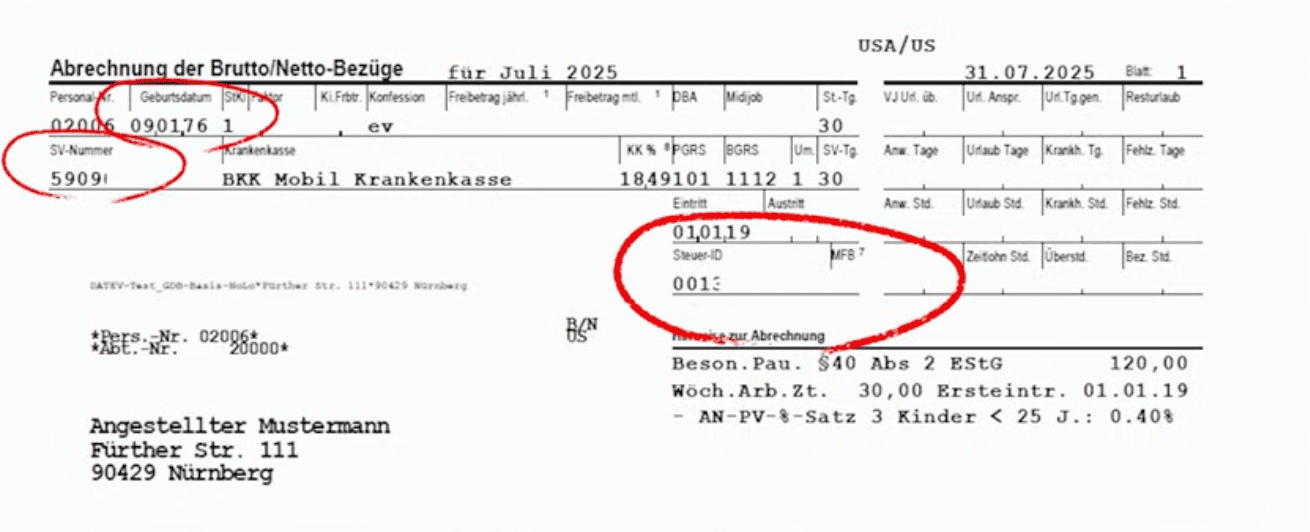

The Header: Your First Line of Defense

Before we dive into the complex math of your gross salary, let’s speedrun the top of your payslip to catch fundamental errors. First, verify your basic identity data: date of birth, Tax ID, and Social Security number. These should never change, but the header also contains dynamic information like your Tax Class (Steuerklasse). If you recently married or your spouse’s income shifted, staying on the default setting can cost you hundreds of Euros in net pay every month.

Next, look for your religious affiliation (Konfession). If it says “ev” or “rk,” you are paying an additional 8% or 9% in church tax—an “optional” deduction that many expats pay for years without realizing they can legally opt out. Finally, check your health insurance provider. With the average Zusatzbeitrag rising to 2.9% in 2026, if your specific Krankenkasse is charging well above this average, it is time to consider a switch to a more cost-effective provider.

Understanding "Geldwerter Vorteil": The Non-Cash Benefit

Once the administrative header is cleared, we look at your total Brutto (Gross). While most focus on their base Gehalt, a great employer often provides “non-cash” benefits known as Geldwerter Vorteil. You might see lines for a Deutschlandticket (JobTicket), which officially costs €63 but is subsidized by your company, or a Home Office Allowance for internet and electricity. Other perks like a JobRad (bicycle leasing) or gym subscriptions also appear here.

Here is the vital part: because these are benefits and not cash, the government adds their value to your gross salary, calculates the tax on that higher total, and then deducts the benefit value before the final payout. This means you might get a “free” gym membership, but your net pay will drop by a few Euros to cover the associated taxes. It’s a net gain in value, but it explains why your bank transfer might look slightly smaller than expected.

Anton vs. Hans: The Progressive Tax Trap

To illustrate how 2026 taxes work, let’s compare two people. Anton earns the average full-time salary of roughly €62,000, while Hans is a high-earner making double that at €124,000. Many expect Hans to simply pay double the tax, but Germany’s progressive system is far more aggressive. Both benefit from the €12,348 tax-free cushion (Grundfreibetrag), which covers a large portion of Anton’s income, keeping his effective tax rate at approximately 16%.

Hans, however, sees the majority of his salary taxed at the top rate of 42%, plus he must pay the solidarity tax (Soli), bringing his effective rate closer to 28%. Consequently, while Hans earns twice as much as Anton, he pays roughly 3.5 times as much in total taxes. This “tax trap” is why high earners in Germany often feel “rich on paper” but struggle to feel the difference in their lifestyle.

Social Security Caps: A Silver Lining for High Earners

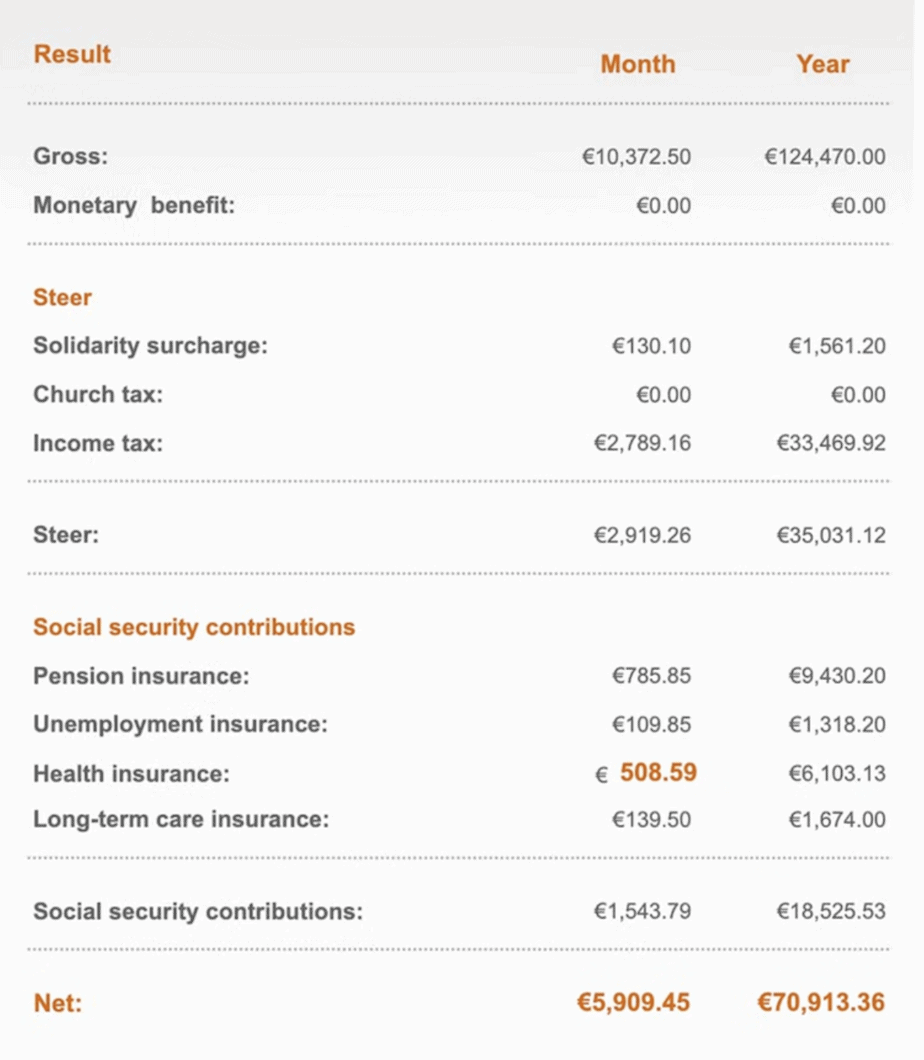

The second block of deductions covers your social security: pension, unemployment, health, and long-term care. For Anton, these are a flat percentage of his entire income. However, Hans benefits from the Beitragsbemessungsgrenze (Contribution Cap). For 2026, the cap for public pension and unemployment insurance is €101,400. Hans earns €124,000, but he only pays contributions on that first €101,400; the remaining €22,600 is free from these specific social charges.

Similarly, the health and long-term care cap is €69,750. While Anton pays health insurance on every Euro, Hans hit the “maximum price” long ago. This explains why Hans pays only about €250 more per month in social security than Anton, despite his massive salary gap. His tax rate is high, but his social security burden as a percentage of income is actually much lower—less than 15%.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe PKV "Cheat Code" for High Earners

Because Hans earns more than the compulsory insurance threshold (€77,400 for 2026), he has a choice that Anton does not: he can leave the statutory system and switch to Private Health Insurance (PKV). In the public system, rates like the 2.9% Zusatzbeitrag are tied to income and keep rising every year. In the private system, premiums are based on age and health status rather than salary.

For high-earning expats, this is often a financial “cheat code,” as it can provide superior medical service for a lower monthly cost than the maximum public premium. If you find yourself in Hans’s shoes—earning above the €77,400 mark and paying the maximum public insurance price—evaluating the switch to PKV is one of the most effective ways to significantly boost your monthly Netto.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe Final Verdict: Real Disposable Income

fSo, what is the final result for our two friends in 2026? Anton, the average-earner, takes home nearly €39,000 Netto, or about 62% of his gross. Hans, despite earning double, keeps only €70,000 Netto, or 57% of his gross. On the surface, it looks like Hans is losing, but a PerFinEx reality check is necessary. In Germany, that “Netto” represents your real disposable income.

Your healthcare, unemployment insurance, and basic pension are already “pre-paid” at the source. Unlike in the US or UK, you don’t necessarily have to deduct massive private insurance premiums from your net pay. Furthermore, Hans has far more leverage to lower his tax burden through smart investments and deductions. Understanding your payslip is the first step; the next is using that knowledge to ensure you aren’t just working for the system, but making the system work for you.