The Ultimate Guide: From Broke to €100,000 in Germany

Ready to build real wealth? Follow our complete guide for expats in Germany to go from broke to financially secure. 🚀

Key Takeaways

- Millions of Germans live paycheck-to-paycheck; this guide provides a step-by-step plan to build financial security.

- The first step is tackling debt. List everything, pay off bad debt, increase income, and cut expenses.

- Prioritize a safety net to cover unexpected expenses and prevent falling back into debt.

- Once secure, transition your mindset to growing money, starting with simple, tax-efficient ETFs.

- The first €100k is the hardest. Accelerate your journey by investing in tax-efficient real estate.

- The game changes. Diversify your investments to protect and grow your wealth while you sleep.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationBuilding Your Financial Fortress

Imagine this: one in four German households has no savings at all—not even €100. That means millions of people are just one unexpected bill or job loss away from serious financial trouble. The good news, however, is that gaining control of your finances isn’t about how much money you have right now; it’s about what you strategically do with it.

This article is your definitive guide, created to show you EXACTLY what to do at every stage of your financial journey, whether you currently have €0, €10,000, or even €100,000. Our goal is to empower you to build real, lasting financial security for yourself and your family, one deliberate step at a time. We understand the unique challenges faced by expats in Germany, from navigating a new banking system to deciphering local financial products.

This guide cuts through the complexity and provides a clear, actionable roadmap so you can move from a state of financial precarity to one of confidence and security. By following these steps, you’ll not only accumulate wealth but also build the strong financial habits necessary for long-term success.

Stage 1: The Debt-Crushing Phase (When Your Net Worth Is Negative)

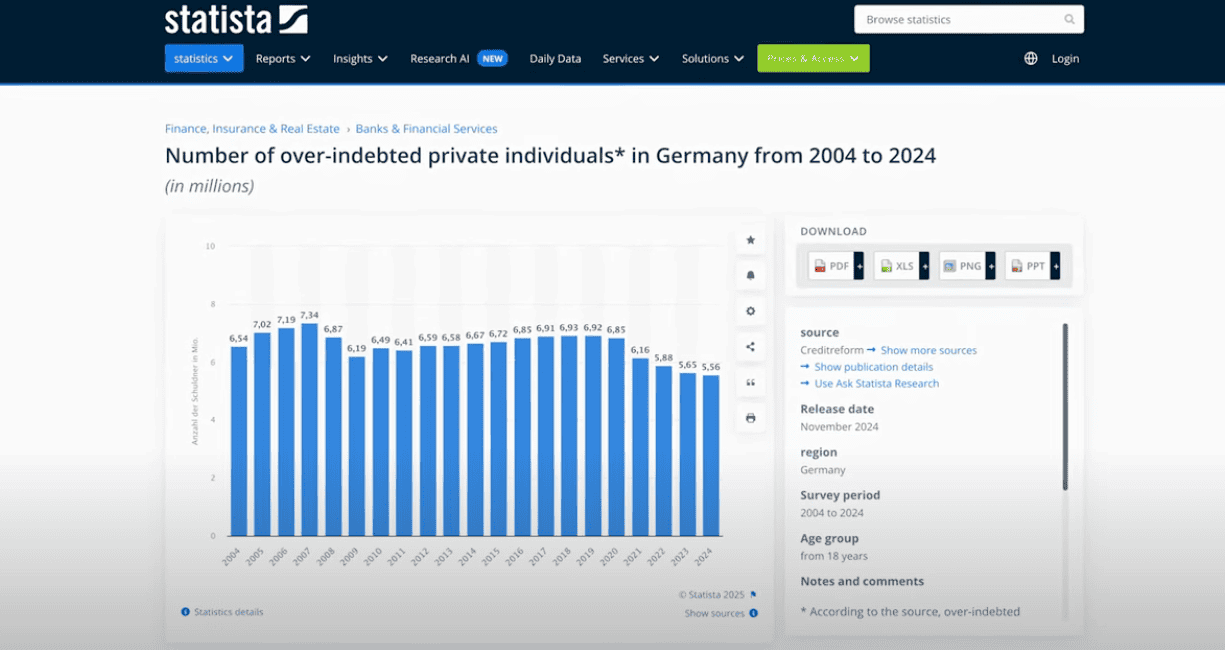

Let’s begin at the very start of the journey, before we even think about building up significant savings. What if you’re in debt and your net worth is actually negative? This situation is more common than you might think, with over 8% of German adults being over-indebted. The good news is that this number has been slowly falling for years, and if you follow these proven steps, you will successfully get out of debt, too.

Let’s be honest—this is, by far, the hardest and most mentally challenging part of the journey from €0 to €100,000. So, your first step is simple but crucial: take a deep breath. Then, list every single debt you have. Include every detail: credit cards, bank overdrafts, “buy-now-pay-later” deals, personal loans—everything. Seeing the full, unvarnished picture of your debt is the first, essential step toward fixing it.

Next, separate what we call “good debt” from “bad debt.” A mortgage on a home you live in? That’s typically good debt. High-interest consumer loans or credit card balances? Those are bad debts. Your top priority is to pay off the bad debt first. Then, you need to cut costs hard. Review every subscription you have, your mobile plan, your insurances—cancel what you don’t genuinely need or switch to more affordable providers. And for the part that really moves the needle: increase your income. Sell unused stuff you have lying around. Start a side hustle. Freelance for a few hours a week. Dog-sit.

Cutting costs has a definite limit, but your potential income is virtually unlimited. Finally, celebrate every small win. Every single debt payment you make is a monumental step forward on your journey.

Stage 2: The Emergency Fund Phase (Building Your Financial Airbag)

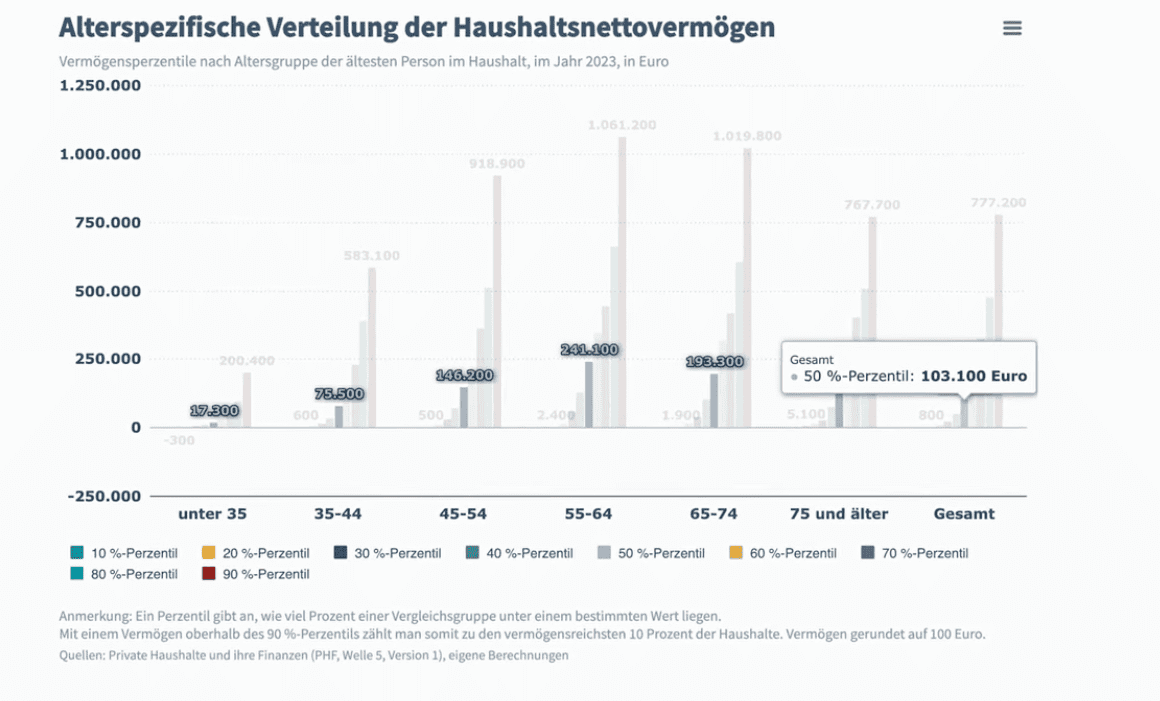

And soon enough, with hard work and determination, you’ll no longer be in debt. You might not have much saved yet, but you’ve reached a new level. Here’s some perspective to motivate you: a net worth of just €800 puts you in the bottom 10% of adults in Germany. It’s a start, but now it’s time to level up.

Your top priority at this critical stage is to build your emergency fund. Think of this as your financial airbag—a crucial buffer designed to cover unexpected expenses without forcing you to fall back into debt. Here’s a simple, actionable rule of thumb we recommend: aim to save 2-3 months of living expenses if you’re single, 4-6 months if you have a family to support, and even more if you are self-employed and your income can be irregular.

Now, a key question for many is: where do you keep this money so you’re not tempted to “accidentally” spend it? The answer is to park it in a high-yield savings account (Tagesgeldkonto) that offers a solid interest rate. This money needs to be easily accessible but not in your daily spending account.

Then, the secret to success here is automation. Set up an automated standing order that transfers a set amount of money right after every payday. Even if it’s just €20, do it. Because consistency, above all else, builds strong financial habits—and those habits are what ultimately build long-term wealth.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationStage 3: The Investment Phase (Shifting Your Mindset)

And once that emergency fund is full and secure, you are ready for your next big move: investing. This is where most people freeze in their tracks because they think, “I don’t have enough money to invest yet.” But the truth is: a couple of thousand Euros isn’t too little—it’s the perfect amount to get started and build confidence.

Your mindset now shifts fundamentally, from simply saving money to actively growing your money. And no, you don’t need to try to pick individual stocks or time the market. The best strategy is to start simple with ETFs—Exchange Traded Funds. They allow you to invest in hundreds or even thousands of companies at once with just a few Euros, instantly giving you powerful diversification. So, set up a monthly savings plan (Sparplan), automate it, and let the immense power of time and compound interest do the heavy lifting for you. But don’t forget the tax side: Germany’s tax system for investments is notoriously complex. Be sure to set up your Freistellungsauftrag with your broker to utilize your €1,000 tax-free allowance on capital gains. This is a crucial step that helps protect you from the infamous Vorabpauschale tax. This tax can apply if your ETF went up in value, even if you don’t sell a single share. And the big issue is that if you sell at a loss later, you don’t get that tax back. It’s a completely ridiculous and frustrating rule, but that’s a topic for another day.

That’s why many smart investors prefer to hold their ETFs within a private pension wrapper (Riester or Rürup plans) instead of a regular brokerage account, as this allows for tax-free growth until retirement. If you’re not sure what strategy fits your goals best, book a free meeting with us. We’ll help you build a plan that works for you, because the earlier you begin, the more time your money has to grow and compound.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationStage 4: The 100K Milestone (The Hardest But Most Rewarding)

Once your basic investments are consistently up and running, your next major milestone is achieving €100,000 in net worth. Statistically speaking, €100k puts you right at the national average in Germany. And that tells us something very important: the first €100k really is the hardest. Why? Because in the beginning, your savings are doing most of the work—your investments aren’t generating massive returns yet. You’re building solid financial habits, not yet profiting from explosive compound growth. But once you hit that €100k mark, your money truly starts working harder than you do.

So, how do you get there faster? For many savvy people, the answer is: real estate. And no, we aren’t talking about buying a massive villa to live in. We’re talking about strategically investing in real estate, such as a small apartment in a solid German city, which helps you build wealth in four powerful ways.

- First is leverage: you use the bank’s money to control a large asset, not just your own.

- Second is cash flow: rental income can cover your mortgage payments or even create a monthly surplus. While maybe not in year one, it should over time.

- Third is appreciation: property values tend to rise over the long term, if you’ve bought the right property in the right location, of course.

- And fourth is tax advantages: Germany offers lucrative tax benefits, including depreciation (AfA), interest write-offs, and zero capital gains tax if you hold the property for 10 years.

In fact, real estate is one of the very few legal ways to actively reduce your taxable income in Germany. Think about it this way: it’s just like the tax-efficient ETFs in pensions we discussed earlier—if the government gives you legal ways to pay less taxes, why wouldn’t you use them? And that’s exactly why so many wealthy people invest in real estate—not just for the returns, but for the profound tax efficiency. The best part is that you don’t need to be rich to start—you just need a plan.

Stage 5: Beyond €100,000 (Structuring Your Wealth)

But if you’re already in the 6-figure club with more than €100,000 in net worth—congratulations. That’s a huge and significant milestone. And now, the game changes once again. At this level, you’re no longer just focused on growing your wealth; you’re strategically structuring it. Because now, your investments do most of the work for you—not your savings. That’s the extraordinary power of compound interest finally kicking in. And the longer you stay invested, the faster your wealth accelerates.

But with more money comes more responsibility. As a famous superhero once said, “with great power comes great responsibility.” That’s where diversification becomes the name of the game. Not just across different asset classes, but also across different risk levels, liquidity, and tax treatments. Start with a solid foundation of broad, low-cost ETFs. Then, build a more sophisticated portfolio and be smart with your position sizing. Real estate becomes even more powerful now. With €100,000 in equity, you can make a serious down payment on a rental property—or even scale into a second one. Bonds might be a great addition for stability and reliable income, especially if you want to de-risk a portion of your capital in the later stages of life. And precious metals like gold and silver can shine brightly during periods of market stress, helping to hedge against inflation and currency risk.

With a €100k net worth, you’re not just investing—you’re building a comprehensive financial system. One that works tirelessly for you while you sleep, travel, or focus on other things in life. And if you want help designing that system—one that is perfectly based on your unique goals, risk profile, and timeline—book a free meeting with us right here. We’ll help you protect what you’ve built and scale it with confidence to the next milestone. Thank you for reading until the very end, and bis zum nächsten Mal!