The Best Way to Invest 2026 (in Germany)

Navigate Germany's 2026 investment paradox with our expert guide. From DAC8 crypto rules to real estate leverage, learn how to keep your profits and retire early! 📈

Key Takeaways

- Balance upcoming tax cuts with new digital reporting rules (DAC8) to keep more of your hard-earned investment returns.

- Learn from “Max Mustermann” to understand average savings rates and how to test investment waters safely.

- Avoid the “Vorabpauschale” trap by using the 1,000€ exemption order or a tax-sheltered private pension wrapper.

- Hold Bitcoin or Gold for over one year to enjoy 100% tax-free profits under German law.

- Use mortgage debt and the 10-year rule to turn tax payments into equity and tax-free capital gains.

- Combine liquidity, tax-freedom, and leverage to build a resilient 2026 portfolio that ensures long-term financial peace.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationHow to Maximize Your Wealth Amidst New German Tax Laws

2026 is an investing paradox for those of us living in Germany. On one hand, the German government is implementing significant tax cuts; on the other, your bank may be taking more money out of your account than ever before. This raises three vital questions: Why are they giving with one hand and taking with the other? How do we stop this leakage legally? And most importantly, is the “Wild West” of German investing officially over now that the Directive on Administrative Cooperation (DAC8) is in effect?.

We have analyzed the three most popular investment strategies for 2026 to show you exactly how to capture those tax cuts and start investing like a professional. By understanding these mechanisms, we can move from being passive participants in the economy to active wealth builders who understand the nuances of the German Finanzamt.

Meeting Max Mustermann: The Average German Investor

To truly understand investing in Germany, we have to look at the most “German” man to ever exist. You have likely seen his name on every sample ID or credit card: Max Mustermann. Today, we reveal his identity to help us build a 2026 strategy.

Max is the average German. He is 45 years old, married with exactly 1.3 children, and drives a grey VW Golf—the most sold car in the country. He earns the average salary of 55,600€ and, like many his age, is sitting on a “mattress” pile of 146,200€ because he is unsure where to put it. With a savings rate of 10.4%, Max is the perfect simulation for our strategies. We will let Max test three different paths so you can learn from his results without risking your own hard-earned capital.

Strategy 1: The ETF Path and the "Vorabpauschale" Trap

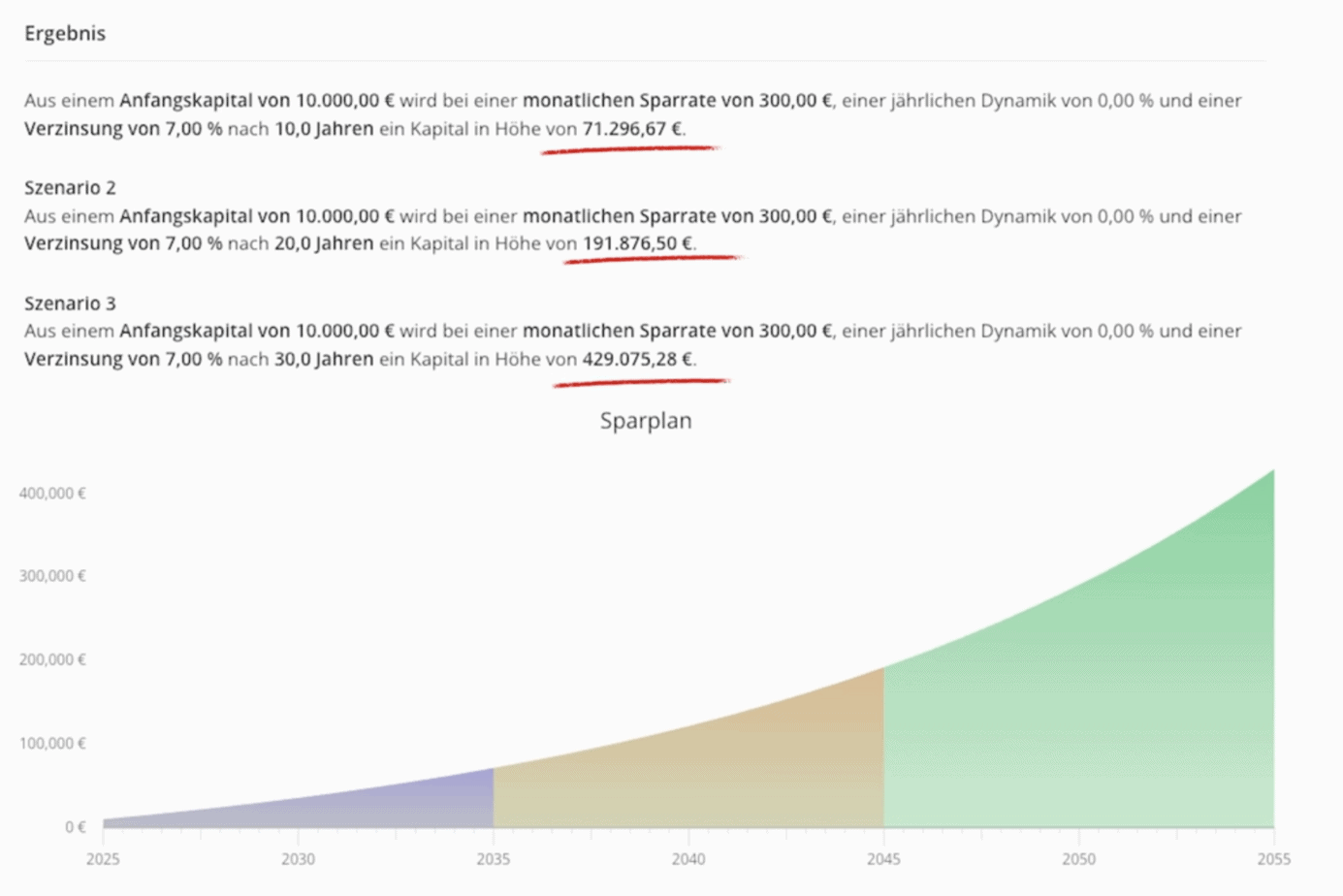

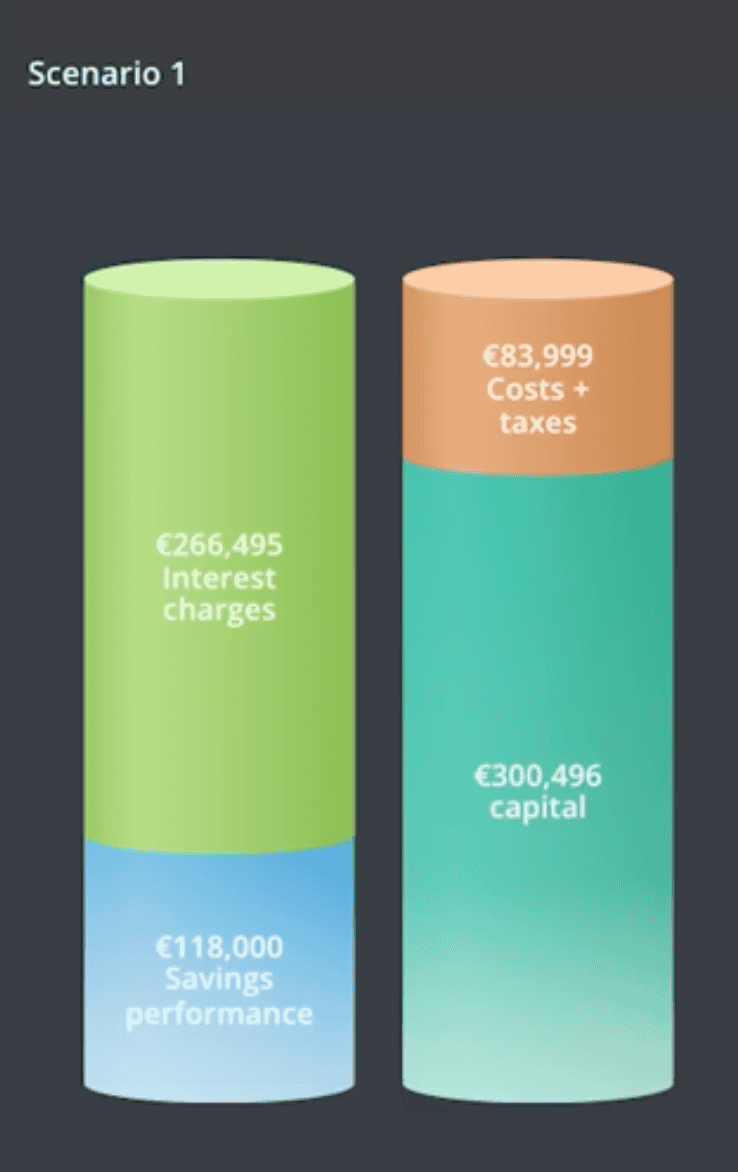

Investment option one is the most popular but often the least tax-efficient: ETFs. “Lazy Max” realizes that with a full-time job and a family, he has zero energy for complex trading. He chooses a “set-and-forget” strategy, putting 300€ monthly into a global diversified ETF. He also moves 10,000€ of his mattress money into a High-Yield Savings Account, currently yielding over 3% interest.

While Max expects his account to grow to 429,000€ over 30 years, the reality is closer to 384,000€. The culprit? The Vorabpauschale. This is a tax on “theoretical” profits that the Finanzamt collects annually. To fix this, we recommend two options: utilizing the Freistellungsauftrag (Exemption Order) for the first 1,000€ of profit, or using a “pension wrapper” to allow the ETFs to grow completely tax-free during the accumulation phase.

Strategy 2: "Hard Money" and the 12-Month Rule

If paying taxes on theoretical profits sounds like a bad joke, meet “Tax-Free Max.” He prefers “hard money” like Bitcoin and physical gold. In Germany, these are not viewed as financial products but as “private assets.” This is the holy grail of German tax law: as long as Max holds these assets for at least one year, every cent of profit is 100% tax-free. While “Lazy Max” might owe over 2,600€ in taxes on a 10,000€ gain, “Tax-Free Max” pays zero.

However, the “Wild West” era is ending. As of January 1, 2026, the DAC8 law forces crypto exchanges to report all holdings and transactions to the Finanzamt. This means total transparency; you can no longer hide your digital wallets. To win here, we must have the discipline to “HODL” for at least 12 months, or we face income tax rates as high as 42%.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationStrategy 3: Real Estate Leverage and the 10-Year Jackpot

Finally, we have “Leverage Max,” who utilizes the most tax-efficient vehicle in Germany: Real Estate. Unlike the others, this Max loves “good debt.” He uses 11,000€ for closing costs on a 200,000€ rental apartment (low in Bavaria at 5.5%) and finances the rest via a mortgage. This strategy works for two reasons.

- Tax Deductions: every Euro of interest, building depreciation, and renovation cost is tax-deductible, effectively lowering his taxable income from his main job.

- The “10-year rule”: if Max sells this property after holding it for a decade, the entire profit is tax-free. If the value doubles, he keeps the full 200,000€ gain, whereas an ETF investor would lose over 50,000€ to the taxman.

The trade-off is illiquidity; you are “married” to the property for ten years, and you must manage tenants and maintenance.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationConclusion: Which "Max" Are You in 2026?

So, which strategy won the simulation? Lazy Max chose peace of mind, Tax-Free Max chose zero tax, and Leverage Max used the bank’s money to build equity. The truth is that there is no single winner. The best investment for us in 2026 isn’t just the one with the highest return on an Excel sheet; it is the one that lets us sleep at night while staying compliant with the new DAC8 and Vorabpauschale rules.

For most of you, the answer is likely a mix of everything—diversification across different tax buckets. Remember, investing is only half the battle; the other half is keeping what you earn from the Finanzamt. By combining these strategies, we can build a resilient portfolio that thrives in the unique German economic environment of 2026.