Inside the Algorithm That Controls Your Life in Germany

Take control of your financial reputation in Germany. We reveal the secrets behind the 2026 SCHUFA update and show you how to build a 999-point perfect score! 🗝️

Key Takeaways

- SCHUFA is replacing its opaque 250-criteria “Black Box” with a clear 12-factor point system in March 2026.

- Loyalty to bank accounts and long-term residential stability are the primary pillars of the new point-based score.

- Frequent new credit cards or “Buy Now, Pay Later” schemes can temporarily damage your active financial reputation.

- Real estate loans and consistent installment repayments act as certificates of trust that boost your overall score.

- Settling outstanding debts within 100 days allows for much faster deletion, offering a fresh start for your record.

- Using “Konditionsanfragen” instead of “Kreditanfragen” keeps your inquiries invisible and your score protected.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe Death of the Black Box: Why 2026 Changes Everything

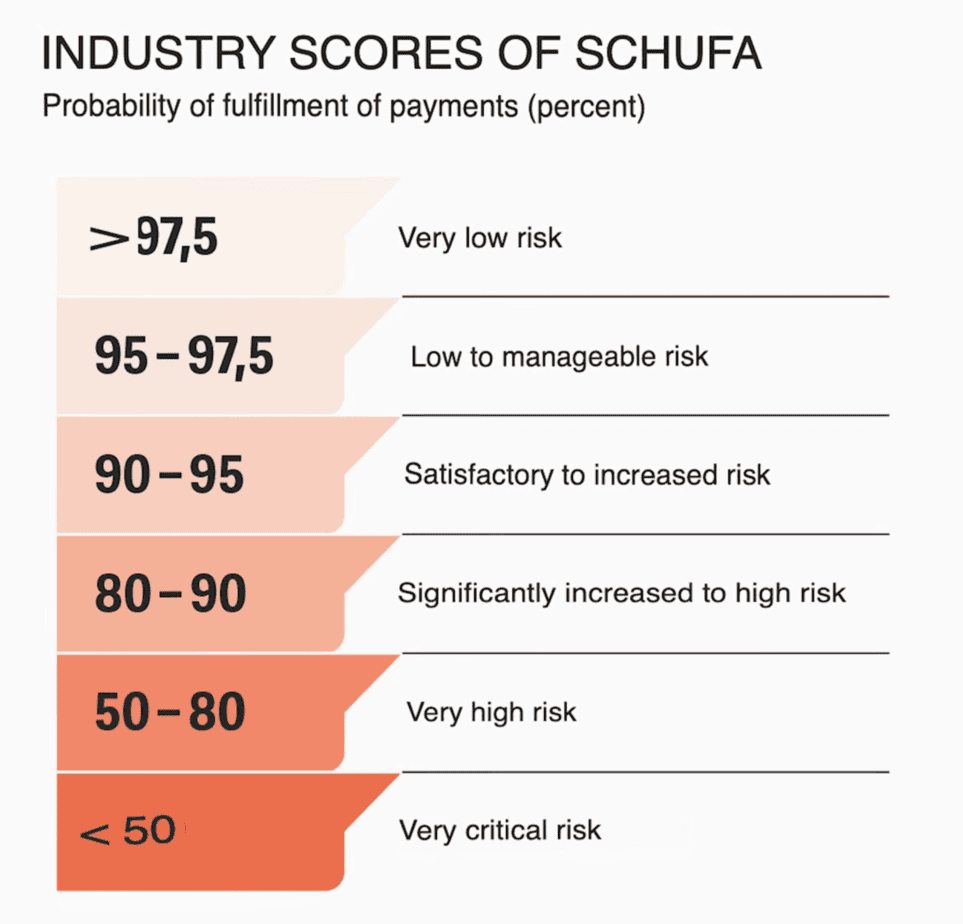

For nearly a century, SCHUFA has operated as the ultimate financial gatekeeper in Germany. Until now, we were judged by a “Basisscore” that felt like a total black box, powered by over 250 criteria. If your score was above 97.5%, you were “excellent”; if it dropped below 90%, banks viewed you with suspicion. The biggest problem for us as expats was the “statistical group” phenomenon—being judged based on the behavior of people in similar demographics because we lacked history.

Starting in March 2026, this “ghost in the box” is being evicted. The new “Next Generation Scoring” introduces a point system from 100 to 999. Crucially, the number we see in our own account will be the exact same number the bank sees. By narrowing the math down to just 12 core criteria, SCHUFA is finally giving us a formula we can actually master.

Group 1: Stability and the Power of Loyalty

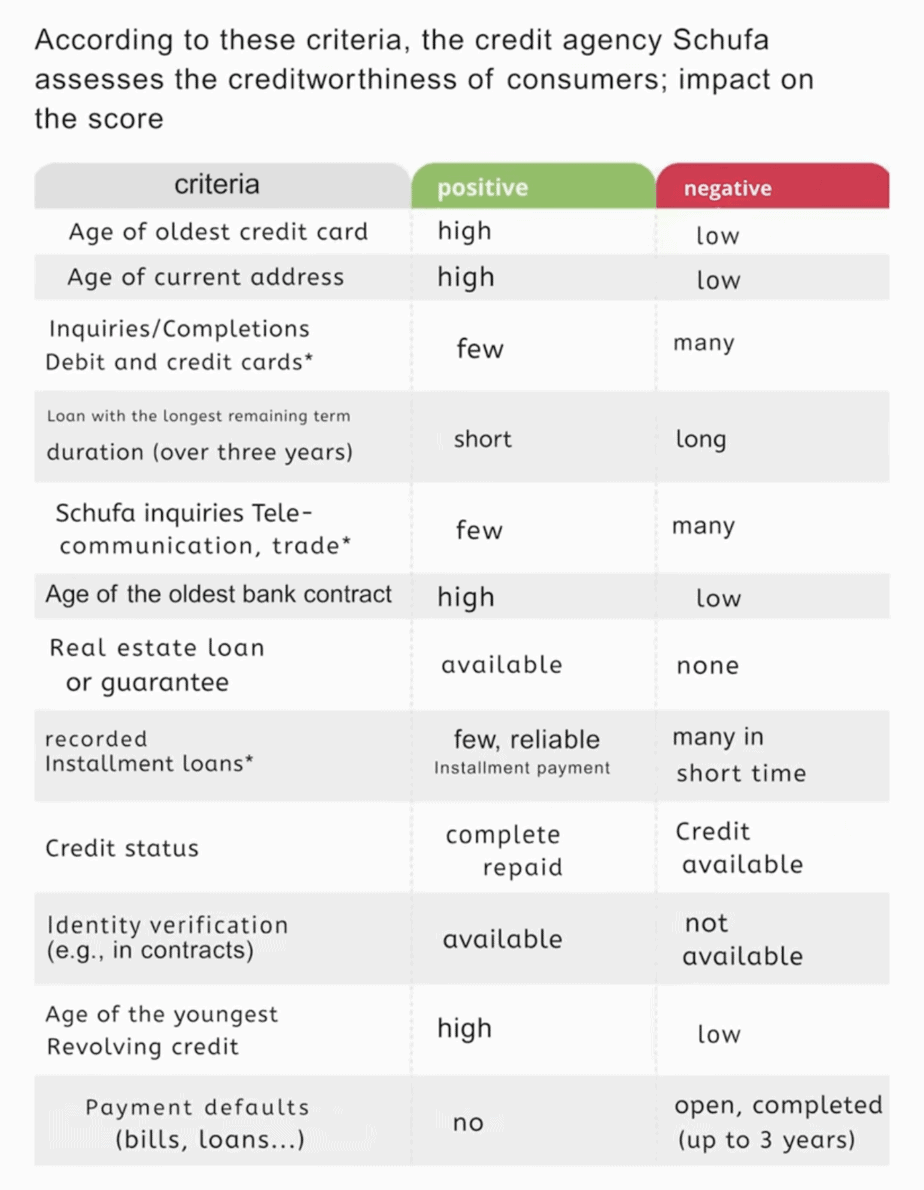

The foundation of your new score is stability. The algorithm essentially wants to know: how long has the German system known you? Loyalty is rewarded here. The age of your oldest bank account and your oldest credit card are two of the 12 critical factors. While it is fine to switch banks for better interest rates—sometimes earning up to 1.5% and significant opening bonuses—changing accounts every few weeks will alert the algorithm.

Furthermore, “Wohnstabilität” is a major factor. Frequent moves in a short period are seen as a risk, while staying at the same address for years builds your point total. Finally, don’t ignore identity verification. Completing processes like Post-Ident or using the online ID function adds a layer of “official trust” that the system rewards with higher points.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationGroup 2: Recent Behavior and the "Buy Now, Pay Later" Risk

While the first group is about your history, the second group looks at your “active” behavior over the last 12 months. This is where many of us accidentally sabotage our reputation. Every time you open a new credit card or a “Dispo” (overdraft) line, you are hunting for liquidity in the eyes of the algorithm. This causes a temporary dip in your score.

Online shopping habits also play a role. Constant use of “Buy Now, Pay Later” services like Klarna or PayPal creates “mini-debts” and frequent inquiries that make your financial life look messy. The heaviest hit, however, comes from payment defaults. If a bill goes to a collection agency, your score will plummet. However, the new system offers a lifeline: if you pay that debt within 100 days, it can be deleted significantly faster than under the old 3-year rule.

Group 3: Debt Management as a Trust Certificate

Surprisingly, the right kind of debt can actually make your score explode upward. Group 3 focuses on debt management and installment loans. For instance, a mortgage is the ultimate certificate of trust. It tells the algorithm that a bank performed a deep-dive audit of your life and decided you were worth a loan of hundreds of thousands of Euros. But be careful: hunting for the best mortgage by making several “Kreditanfragen” (credit inquiries) can hurt you. We recommend using a broker like us who can query hundreds of banks with a single “Konditionsanfrage,” which remains invisible to the algorithm.

The new scoring also looks at your current installment loans and their remaining terms. If you repay them on time every month, your score will often be higher than someone with no credit history at all, because you are proving you can handle responsibility.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe Secret Sauce: Why Weighting Matters

Even though the 12 criteria are now public, SCHUFA still keeps its “secret sauce” hidden. They have revealed what they look at, but they refuse to say how much each factor is weighted in the final 100-999 formula. This is intended to prevent people from “gaming” the system by opening or closing accounts purely for points.

However, knowing the ingredients allows us to influence the recipe. For example, knowing that “payment status” and “ident verification” are on the list means we can proactively address them. We might not know if residential stability is 10% or 20% of the score, but we know it is a factor that we should prioritize when planning our next move.

Three Steps to Take Before March 2026

To ensure you are ready for the March 2026 rollout, follow this three-step strategy today.

- Request your free “Datenkopie” (data copy) under Art. 15 GDPR to check for errors. Even a single wrong entry can block a future loan. If you find an old, unpaid bill, settle it immediately to trigger the 100-day deletion rule.

- Protect your inquiries. When comparing loans, always insist on a Konditionsanfrage so your score stays protected.

- Get your digital registration ready for the new SCHUFA portal. There will likely be a waitlist, and being among the first to see your new point-based score will give you the lead time needed to make any necessary adjustments.

Germany is finally handing us the keys to our own financial data; it is time we learn how to use them.