Germany 2026: Financial Changes for Expats – Costs Rising by Double Digits?

Your guide to Germany’s 2026 financial shake-up: learn how tax breaks, pensions, and health insurance costs will hit your wallet. 💰

Key Takeaways

- Germany 2026 brings mixed financial news; while some costs rise sharply, opportunities exist to earn more and save on taxes.

- The Kindergeld and Kinderfreibetrag will both see slight but non-impactful increases, mainly offsetting minimal inflation.

- The highest 42% tax bracket threshold rises to €69k, allowing high earners to keep more income before hitting the top rate.

- The Steuerfreibetrag rises by almost €300, ensuring every person keeps a larger portion of their income untaxed.

- The max. income cap for pension and unemployment contributions rises significantly to €101k, increasing costs for high earners.

- The income cap for health and care insurance rises, and the Zusatzbeitrag is increasing sharply, boosting monthly premiums.

- The income threshold to leave the public system jumps to €77k, making private insurance less accessible for moderate high earners.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationBreaking Down the Major Financial Shifts for the New Year

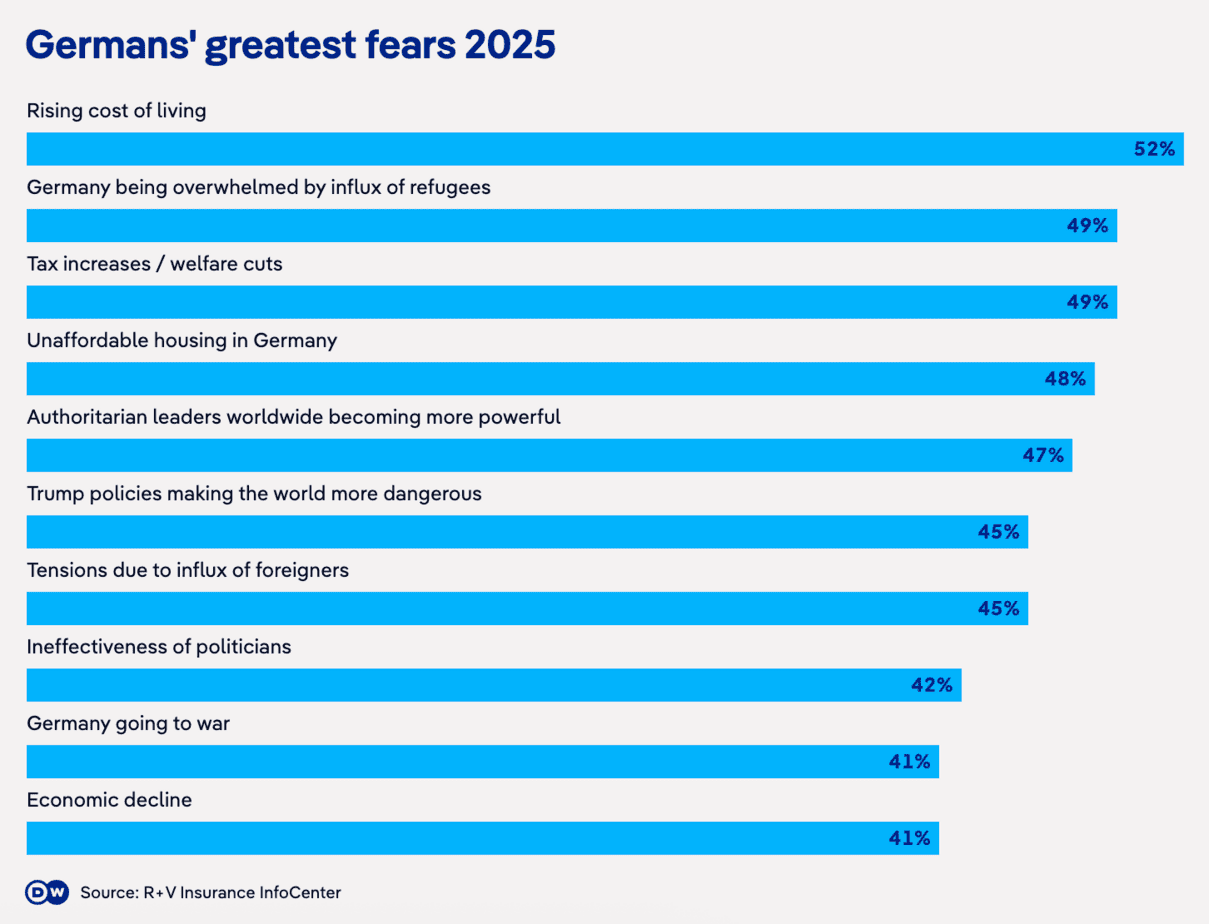

The financial landscape in Germany for 2026 is poised to hit your wallet harder than you might expect, with some costs set to rise by double digits. No wonder that “rising cost of living,” “tax increases,” and “welfare cuts” rank among Germans’ top worries. However, it is not all bad news. While some costs inevitably rise, you can also benefit from earning more money and paying less in taxes.

As is usually the case, if you pay more on one end, you can strategically save more on another end, especially if you follow a comprehensive financial plan. So the crucial question is: Will you pay more next year, and if so, how much? We will go step-by-step through every major financial change so you are not surprised when your January paycheck arrives.

Tax Relief: Modest Adjustments for Families

For expat families, there are minor adjustments coming in 2026 that may offer slight relief. First, the Kindergeld—the monthly child benefit—will rise slightly by €4 per month. Every Euro helps, but this small bump won’t make much difference when inflation alone was 2.3% last month. Therefore, think of it as a polite adjustment intended to offset minor cost increases rather than a real financial relief for families.

And there is one more update for parents: the Kinderfreibetrag—the child tax allowance that reduces how much of your income is subject to tax—will also rise, albeit ever so slightly. That means a little more of your income stays tax-free, but the overall effect on your net pay remains minimal. What’s far more noticeable is the next change, because in 2026, many individuals will effectively pay less in income tax due to the shifting of tax brackets.

Income Tax Relief: Shifting Tax Brackets

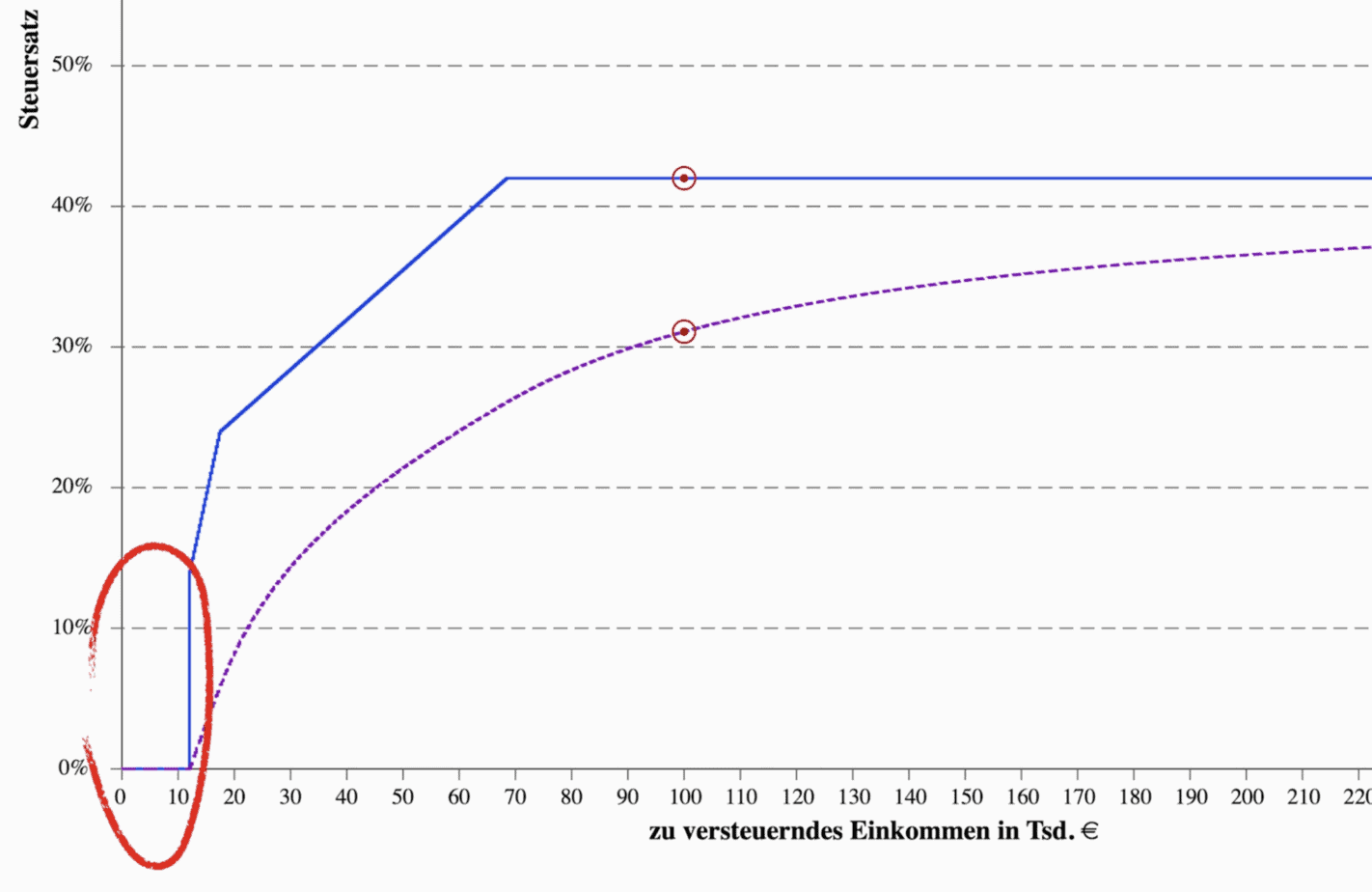

Here in Germany, we have a progressive income tax system: the more you earn, the higher your tax rate. We track two rates: the marginal tax rate, which is what you pay on your last Euro of income, and the average tax rate, which reflects what you pay on all your income combined. The key change for 2026 focuses on the top tax brackets. The highest 42% marginal tax bracket starts at €68,000 in 2025, but in 2026, it shifts up to €69,000, an increase of 2.04%.

This means that while the tax rate itself does not change, the limit moves higher, allowing you to earn a little more before reaching that top bracket. If you are in this high-tax category and wondering how you can further optimize your income for 2026, we can show you exactly how to leverage tax-advantaged vehicles in a free one-on-one meeting. There are all kinds of ways to save taxes, but your maximum benefit will always be capped at the marginal rate of 42%.

Income Tax Relief: Basic Tax-Free Allowance

The Steuerfreibetrag, or basic tax-free allowance, is the amount every single person in Germany can earn without paying a single cent in income tax. It is designed to ensure that a basic part of your income stays completely untaxed, guaranteeing that everyone keeps at least a small portion of their earnings, no matter how much they make. This allowance is set to rise by almost €300 in 2026. This represents a tangible benefit for all taxpayers, especially those at the lower and middle-income levels, as the increase directly boosts their take-home pay.

Unfortunately, this is where the good news regarding tax savings largely ends. No more modest adjustments that offset inflation and boost your net pay. Because now that we move from taxes to social security, those percentages—and, more importantly, the income caps to which they apply—will start taking money out of your pocket instead of putting it back in.

Rising Social Security Caps: Pension and Unemployment

Before addressing health insurance, let’s first look at Germany’s public pension and unemployment insurance. All four insurances of the German social security system are calculated in a very similar way.

The contribution rate for the public pension stays at 18.6%, split equally between employee and employer. That rate itself does not rise, which is the good news. But 18.6% of what is the real question. This is where the maximum income level to calculate your contributions, called the Beitragsbemessungsgrenze, comes into play. You pay social security contributions only up to that limit; everything you earn above it is not charged anymore.

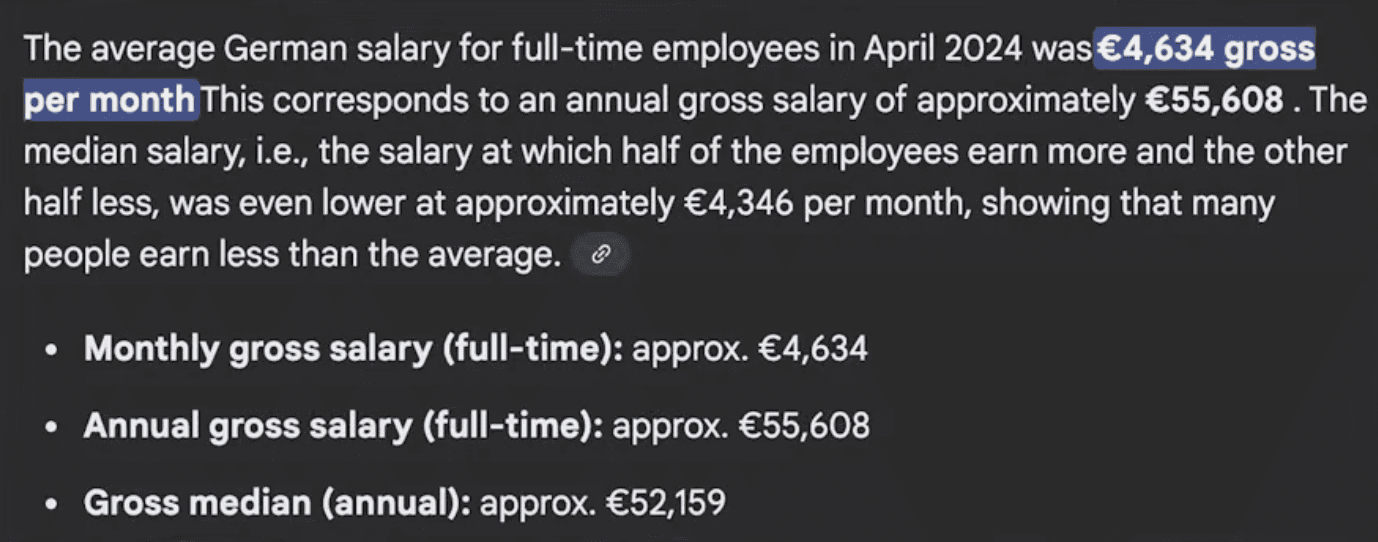

Because that limit moves higher, your total contribution does too. In 2025, that limit for public pension and unemployment insurance is €96,000, and in 2026 it rises to €101,000. If you earn the average German salary of about €55,000, you won’t notice any difference. However, if your salary is above the new cap of €101,000, you will be fully affected, paying over €70 more per month than this year. Since unemployment insurance follows the same pattern, its maximum contribution also rises by almost 5%.

Rising Health & Care Insurance Costs: Hitting the High Earners

Now, let’s move to what many of you have been waiting for—health insurance. Compared to taxes and pensions, this is where the real cost increases happen in 2026. Just like with the public pension, health insurance also has a maximum income limit for calculating your contributions. Since that limit moves up every year, your payments automatically go up too, at least if your salary is high enough.

In 2025, the income limit for public health insurance is €66,000, and in 2026 it rises to €69,000. Care insurance (Pflegeversicherung), which shares the same income limit, will see its monthly contribution rise by exactly 5.44%. While not huge in Euros, these quiet percentage bumps add up fast, especially when multiple insurances rise at once.

Public health insurance is getting significantly more expensive. The general contribution rate stays the same at 14.6%, but because it’s applied to the higher income limit, the monthly cost rises by almost 8%. For the first time in German history, the maximum contribution for public health insurance will cost over €1,000 per month.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe Big One: The Additional Health Contribution (Zusatzbeitrag)

If you paid close attention to the numbers, something doesn’t fully add up: why does care insurance rise by 5% but health insurance by 8%, even though both are tied to the same income limit?

Great question—it means there’s more behind this. In public health insurance, you don’t just pay the general 14.6% contribution; you also pay the additional contribution—the Zusatzbeitrag. This is the extra percentage each Krankenkasse (health insurer) can charge on top of the base rate. On average, the Zusatzbeitrag is rising to 2.9% next year. That may sound small, but it’s a 16% increase to the Zusatzbeitrag itself. This is the primary driver for the increased cost, and it’s why you’ll pay more than ever before in 2026 for the same level of coverage in Germany’s public health insurance.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe High Barrier to Private Health Insurance

Given these rising costs, some of you might wonder if there is a way out of all this. Yes, if you are allowed to switch to private health insurance. For that, your salary has to exceed the Jahresarbeitsentgeltgrenze—the annual income threshold for leaving the public system. In 2025, it is €73,800, and in 2026 it jumps significantly to €77,400. That means you will need to earn at least €3,600 more per year just to qualify for private health insurance.

This substantial jump makes switching much harder for moderate high earners. If you do earn that much and wonder whether switching to private is a smart move for your personal financial planning, you can book a free meeting with us. Understanding these thresholds is key to managing your financial health in Germany.

Pingback: Germany 2026: The Complete Guide to Financial, Work, and Visa Changes

Pingback: Germany February 2026: Big Financial Changes for Expats & Investors