The 10 Most Expensive ETF Investing Mistakes (And How to Avoid Them)

ETF investing is easy... and easy to get wrong! Learn the 10 most expensive mistakes and how to avoid them. 💸

Key Takeaways

- While seemingly easy, ETF investing has hidden traps. This guide reveals 10 costly mistakes to help you build real wealth.

- Avoid blindly following trends or social media advice; instead, build your own personalized investing strategy.

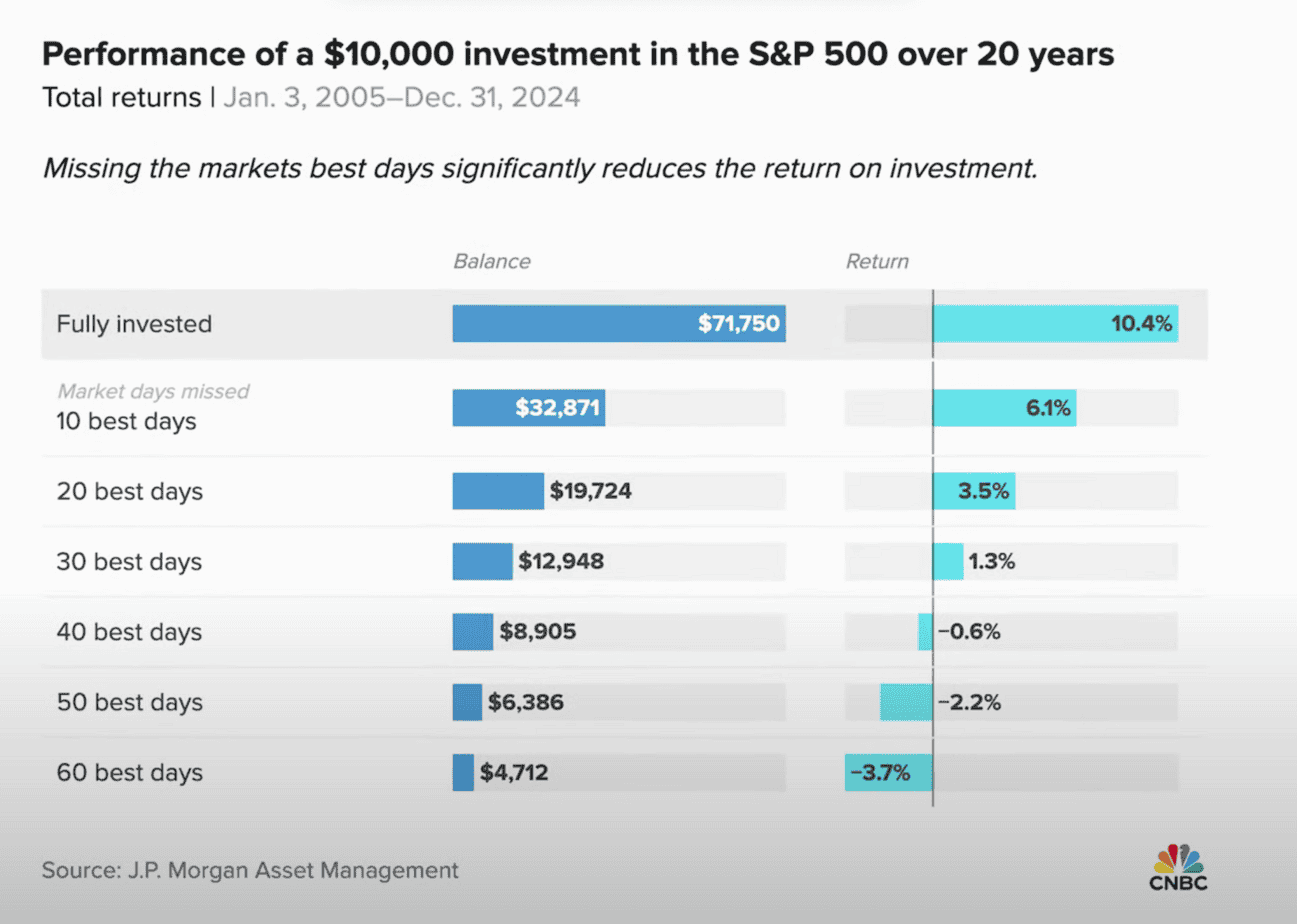

- Consistently timing the market is impossible. Focus on time in the market to benefit from long-term compound growth.

- Never invest your emergency fund; always maintain a separate cash reserve to avoid forced selling during downturns.

- Avoid leveraged ETFs for long-term investing; daily resets can cause them to underperform even rising markets.

- Holding multiple overlapping ETFs is not true diversification; ensure your portfolio is spread across different markets.

- Neglecting to rebalance your portfolio can quietly shift your risk, so check and adjust periodically to maintain your target allocation.

- Forced ETF mergers can trigger capital gains tax; holding ETFs in a pension wrapper can offer tax-free growth.

- Failing to use your tax-free allowance or ignoring the Vorabpauschale can cost you thousands in unnecessary taxes.

- The biggest mistake is waiting for the perfect moment; start now, start small, and let compound interest do the work.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe "Passive" Trap: How Unwise Choices Sabotage Your Financial Future

Investing in ETFs is often praised for its simplicity—you can buy them with just a few clicks, just like this. But if it’s so easy, why do most investors still lose money? The simple truth is: “passive” doesn’t mean “mistake-proof.” You might be unknowingly sabotaging your financial future, and it could be costing you thousands of Euros in the long run.

To ensure this doesn’t happen to you, we’ve put together a comprehensive guide to the top 10 most expensive ETF investing mistakes. We’ll break down each one, explain why it’s so costly, and give you clear, actionable steps on how to avoid it entirely. Our goal is to empower you to invest with confidence, build a robust portfolio, and achieve real financial security. By the end of this article, you’ll have the knowledge you need to navigate the world of ETFs like a seasoned professional, sidestepping the pitfalls that trap so many others.

#1: Herd Mentality & #2: Trying to Time the Market

One of the most common—and most costly—ETF investing mistakes is falling for herd mentality. Many people start investing without a clear, personalized strategy. Instead, they just buy what’s trending, what some random influencer hypes on social media, or what someone on Reddit recommended. The problem is that these tips almost never align with your unique goals, your personal risk tolerance, or your time horizon. Instead of understanding what they’re actually buying, many beginners jump into a niche ETF like clean energy, AI, or gaming, often after the hype has already peaked. And when the market inevitably drops, they panic-sell, locking in losses.

That’s a perfect example of mistake number two: trying to time the market. It sounds smart, right? You wait for the perfect dip to buy and then sell right at the top before the next crash. But here’s the uncomfortable truth: you might get lucky once or twice, but no one—not even professionals—can get this right consistently. Financial markets are complex and unpredictable, and by the time news of a crash or a recovery hits you, it’s already priced in. Jumping in and out of the market doesn’t just rack up costs, taxes, and stress; missing just a few of the best-performing days can absolutely destroy your long-term returns. If you invest €10,000 into the S&P 500 for 20 years, you could end up with over €71,000. But if you miss just the 10 best days, you’d have less than half of that. So, forget about perfect timing. Your focus should be on time in the market, not timing the market. Just find a good broker and get started.

#3: Investing Money You Need Soon & #4: Chasing Too Much Return

When we’re talking about emotional investing, we have to mention mistake number three: investing money you might need soon. It’s incredibly tempting to invest every single Euro you have to chase higher returns, and we understand that impulse. But here’s the danger: if you put your emergency fund into ETFs, you risk being forced to sell when the market is down. Unexpected costs happen all the time—a broken fridge, a sudden job loss, or a surprise tax bill. And if you don’t have cash on hand, you’ll be forced to sell your ETFs at a loss to cover the bill. So, here’s a crucial rule: only invest money you won’t need for at least 10 years. Before anything else, focus on building a solid emergency fund. Right now, you can get a great interest rate with top savings accounts in Europe, which ensures your money is safe and accessible.

Speaking of chasing high returns, the next mistake comes from investing in leveraged ETFs. On the surface, they sound great: if the market goes up 1%, a 2x leveraged ETF goes up 2%. But if the market drops 1%, you lose 2%. And it gets even worse. Leveraged ETFs reset daily. They multiply each day’s return, not the overall trend. So, if the market goes up 1% one day and down 1% the next, a normal ETF ends up about where it started. But a 2x ETF amplifies both moves and ends up below where it began. These daily swings add up, and over time, leveraged ETFs may fall behind the regular ETF, even if the market is rising. They are meant for short-term trading, not long-term investing. If you want to start long-term investing but aren’t sure where to begin, book a free meeting with us. We’ll help you invest with confidence and avoid these costly mistakes.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information#5: The Illusion of Diversification & #6: Not Rebalancing Your Portfolio

Now let’s talk about the illusion of diversification. Many investors mistakenly believe that more ETFs automatically mean more diversification and greater safety. But in reality, that’s not always true. For example, you might hold a broad MSCI World ETF and an S&P 500 ETF, thinking you’re well-diversified. But both ETFs include the exact same top companies, and in fact, they overlap by a staggering 54% because the MSCI World already contains all the companies in the S&P 500. That’s not diversification; that’s duplication. True diversification means spreading your risk across different regions, sectors, and market sizes, not just owning more ETFs that hold the same things.

So, you’ve picked well-diversified ETFs and spread your risk, but then you forget about them completely. That brings us to the next big mistake: not rebalancing your portfolio. Just because ETFs are passive doesn’t mean your portfolio is on autopilot. Over time, different parts of your portfolio will grow at different speeds. For example, a tech-heavy ETF might boom while a dividend-focused one falls behind, or vice versa. Imagine you started with a 50/50 split, and then over time it drifts to 70/30 or even 90/10. If you don’t rebalance, your risk profile slowly shifts. What began as a balanced strategy can quietly turn into a high-risk portfolio without you even noticing. The simple fix is to check your allocations every once in a while and bring them back to your target. We usually do this by simply adjusting our monthly savings plans, because selling parts of a portfolio would trigger taxes—and we prefer to avoid taxes whenever we legally can.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information#7: Ignoring Tax-Smart Investing & #8: Overlooking German Tax Rules

Did you know that investors in Germany can be forced to sell an ETF and pay taxes on it, even if they never wanted to? That’s the next mistake. In early 2025, one of Amundi’s biggest ETFs, the Amundi MSCI World V, was merged into another ETF. Thousands of investors were forced to sell, even though they didn’t want to. Why? Because the merger legally triggered a capital gains tax. So, even if you didn’t touch your ETF, you still had to pay taxes and maybe even sell part of your portfolio just to cover the tax bill. There was one important exception: investors who held the ETF inside a tax-advantaged pension plan paid zero taxes on the transaction. This highlights a crucial point: investing is a long-term game, and being tax-smart is key to winning.

This brings us to mistake number eight: overlooking German tax rules. Here in Germany, capital gains, interest, and dividends are taxed at 25% plus solidarity tax, and maybe even church tax on top. And yes, even accumulating ETFs that reinvest profits trigger a tax through something called the Vorabpauschale, which you can only legally avoid inside a pension wrapper. The good news is that every investor has a tax-free allowance of €1,000 per year (€2,000 if you’re married). But this only works if you set up a Freistellungsauftrag with your broker. Failing to do so means you’re giving away thousands in tax savings over time.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information#9: Investing in Currency-Hedged ETFs & #10: Never Getting Started

Taxes are a big cost, but you know what else is costly? Investing in currency-hedged ETFs. They sound safe because “hedged” implies protection. But for most long-term investors, they just add extra cost without any real long-term benefit. These ETFs charge higher fees and often include hidden costs that you’ll never see on a statement. Over time, currency movements in a globally diversified portfolio usually balance out naturally. A company like Apple, for example, trades in dollars but earns revenue globally, so it already has a built-in currency diversification. Many investors also confuse the trading currency of an ETF with a currency hedge. Just because an ETF is priced in dollars doesn’t mean it’s inherently risky for Euro investors; your broker automatically handles the exchange rate. Unless you’re investing in foreign bonds or niche markets, you probably don’t need a hedge. Our advice is to stick to globally diversified, unhedged ETFs and keep it simple.

And finally, the biggest and most expensive mistake of all: never getting started. People spend years trying to find the perfect strategy, the perfect timing, or wait for the perfect moment. But waiting is incredibly expensive. Every year you sit on the sidelines, you miss out on the incredible power of compound interest, and you give inflation more time to quietly eat away at your savings. Some people are afraid of doing it wrong. Others think they need to know everything first. But the best way to learn? Start. Start small. Start imperfectly. Just… start. If you’re unsure how to begin or want someone to help you start smart, book a free meeting with us. We’ll walk you through it, step by step. Thank you for reading, and bis zum nächsten Mal!

Pingback: Where Germany Spends YOUR Taxes: The 2026 Budget vs. Reality

Pingback: Best Broker for Expats in Germany 2026: Trade Republic vs. ING vs. IBKR