The 7 Hidden Costs of Buying a Property in Germany

Buying a home in Germany? We reveal the 7 hidden costs you didn't know about so you can plan your budget right! 🏡

Key Takeaways

- Homebuyers often forget major costs; we’ll reveal all hidden expenses to prevent you from making an expensive mistake.

- Upfront costs like real estate transfer tax, notary fees, and commissions can add up to 15% of the purchase price.

- Be aware of hidden costs beyond the interest rate, such as commitment interest and mortgage registration fees.

- Hiring a professional inspector and budgeting for mandatory renovations can save you tens of thousands of Euros.

- Don’t forget to budget for the move itself, new furniture, and the monthly operating and maintenance costs of homeownership.

- Selling costs like a prepayment penalty and speculation tax can catch you by surprise and severely reduce your profits.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationDon't Get Caught by Surprise: A Complete Guide to German Property Costs

Most homebuyers in Germany forget at least three major costs when signing the contract, and by the time they find out about them, it is already too late. We can almost guarantee you don’t know them all either, and they could catch you by surprise too. Imagine saving for years to buy your dream home, only to realize you cannot afford it because of costs nobody told you about.

To make sure this doesn’t happen to you, we’re going to show you all of the hidden costs of buying a property in Germany. We want you to be able to plan ahead and avoid what could be the most expensive mistake of your entire life. Understanding these costs is the first and most critical step toward making a smart and secure real estate investment.

Hidden Cost 1: Incidental Costs

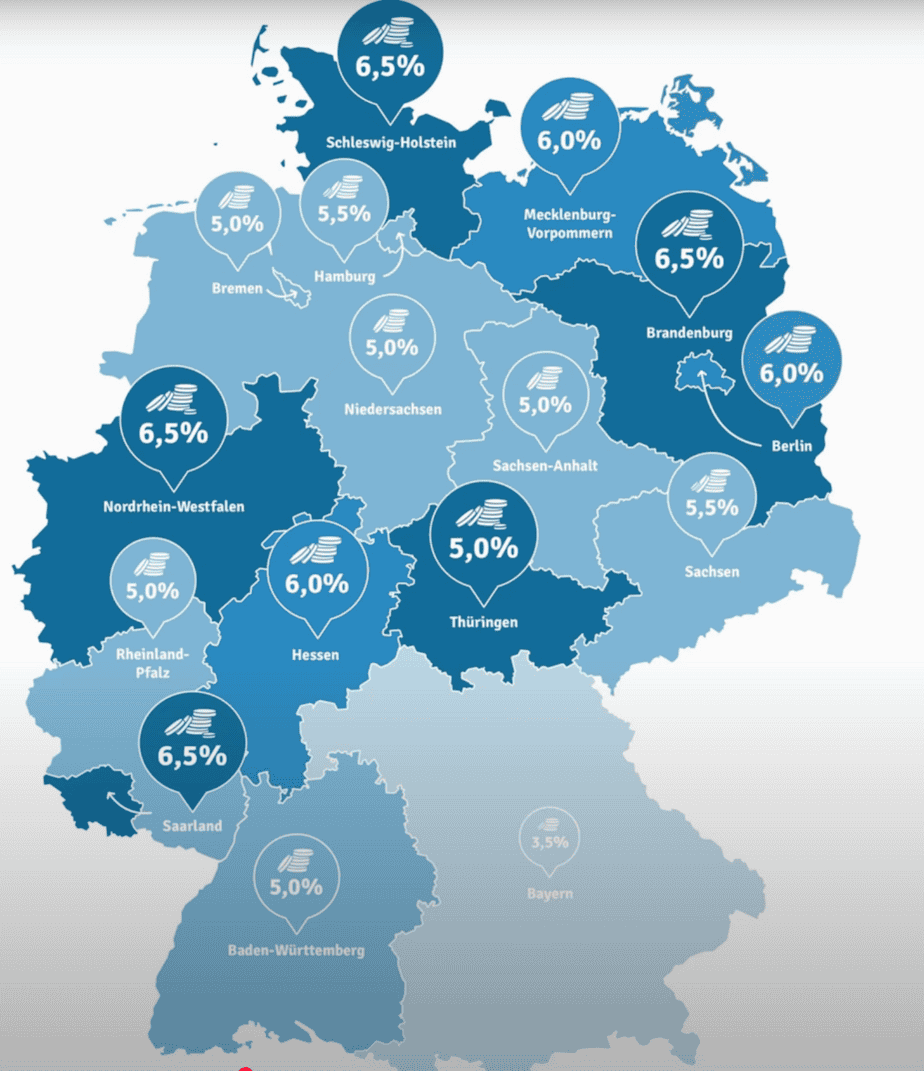

The first and most significant hidden costs are the Kaufnebenkosten—the extra costs on top of the property price. These usually add up to 10% to 15% of the property’s value, and banks often will not finance them. So, you’ll need to cover them with your own savings. The biggest part of this is the real estate transfer tax, or Grunderwerbsteuer in German. Depending on the state, this ranges from 3.5% here in Bavaria up to 6.5% in states like Brandenburg. On a €400,000 home, that’s up to €26,000 gone before you even get the keys.

Then come the notary and land registry fees. Both are legally required, both are set by law, and together they add around 2% of the purchase price. And finally, there is the real estate agent commission. If an agent is involved, expect another 3% to 7% of the purchase price. All in all, Kaufnebenkosten can easily cost you tens of thousands of Euros on top of the property price, and you’ll need that money in cash.

Hidden Cost 2: Financing Fees & Hidden Mortgage Traps

The second hidden cost is financing. These are all the extra fees that come with your mortgage, beyond the interest rate, and they can add up quickly. First is the mortgage registration fee (Grundschuldbestellung) at the notary. This is the legal security your bank needs, and it usually costs around 0.5% of the loan amount.

Second are commitment interest fees (Bereitstellungszinsen). They kick in if your loan is approved, but you don’t use it right away, which often happens with new constructions. After a free period of 6 to 12 months, banks typically charge 0.25% per month on the unused loan. That can get very expensive if your property is delayed.

Third are miscellaneous loan fees. Some banks still charge for account management, property valuations, or even copies from the land register. These may sound small, but together, they can cost hundreds or even thousands of Euros. So don’t just compare interest rates; find the right bank that will save you a lot of money on these hidden financing costs.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationHidden Costs 3 & 4: Experts & Unexpected Renovations

The third hidden cost is expert reports. Hiring an independent expert might sound optional, but in reality, it can save you from massive surprises later on. If you’re buying an existing home, a building inspector can uncover problems you would probably miss. Things like moisture in the walls, roof damage, outdated electrics, or even asbestos in old materials. These issues can easily cost you tens of thousands of Euros if you discover them too late. A professional inspection usually costs a few hundred to €1,000, but compared to the risk, it’s money well spent. If you’re building a new home, it’s also smart to bring in an independent expert during construction to check the quality of the work.

The fourth hidden cost is renovation, which is especially important if you’re buying an older property. In Germany, there are even legal modernization requirements. If you buy an old house, you might have to replace outdated oil or gas heating by law, and you only get two years after purchase to complete this work. Ignore it, and you risk hefty fines of up to €50,000. Then there are the hidden damages: mold, asbestos, or outdated electrics and plumbing. Renovation costs add up fast. A new heating system alone can cost €15,000. And a full renovation can easily be hundreds of thousands of Euros for a typical house. That’s why it’s so important to budget for renovations in advance.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationHidden Costs 5 & 6: The Move and Monthly Expenses

The fifth hidden cost is moving. And while it may sound obvious, most buyers completely forget to budget for it. Hiring a moving company can easily cost €2,000 or more, depending on the distance and effort. Once you’re in your new place, chances are you’ll need new furniture, curtains, or maybe even a brand-new kitchen. A kitchen alone can easily cost €10,000 or more. On top of that come the utility connection fees. Setting up electricity, water, internet, or gas usually adds another few thousand Euros. So while moving may feel like the smallest part of the process, it can still cost you tens of thousands of Euros extra.

The sixth hidden cost is operating expenses. Buying the property is one thing, but keeping it every month is another. These costs come in two categories: fixed and variable. Fixed costs include the annual property tax, waste collection, and insurance. Property tax alone can run several hundred Euros per year. Home insurance is another big one, usually €200 to €700 per year. And then there are the maintenance costs. Every roof, heating system, or bathroom eventually needs replacing. A good rule of thumb is to set aside at least 1% of the property value per year. For a €400,000 home, that’s €4,000 every single year. So don’t just calculate the purchase price. Your property will keep costing you money long after you move in.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationHidden Cost 7: Selling, Taxes & Prepayment Penalties

And the seventh hidden cost is selling. This one often catches people completely by surprise because you only notice it when you want to get out. The first one is the prepayment penalty, or Vorfälligkeitsentschädigung in German. If you pay off your mortgage early—before the fixed interest period ends—the bank can charge you a hefty fee. Why? Because they lose the interest income they were counting on. And depending on your loan size and remaining term, this penalty can be tens of thousands of Euros.

The second one is the speculation tax, or Spekulationssteuer. If you sell a property within 10 years of buying it and you haven’t lived in it yourself, any profit you make is taxed as income. That means if you sell an investment property after 8 years with a €100,000 gain, up to 42% of your profit goes straight to the tax office. Remember: buying a property is not just about the entry costs but also about the right exit strategy. We can help you create a plan to avoid these costly mistakes.