Can I Afford This Property With My Salary?

Thinking of buying a home in Germany? Learn how much property you can actually afford — and avoid costly mistakes 🏘️

Key Takeaways

- Buying more home than you can afford can be a financial disaster — learn how banks and you should calculate it.

- Your net income is the foundation of how much you can borrow — and spend — on real estate in Germany.

- To buy property, you’ll need up to 20% of the home’s value in cash — and banks rarely cover that.

- Even a 1% increase in mortgage interest can cost you tens of thousands of euros over the loan’s lifetime.

- With 3,000€ net income and 20k€ savings, a single buyer might afford up to a 220,000€ property — with full financing.

- A couple earning 5,000€/month with 80,000€ savings can afford a 300k–440k€ home depending on their risk tolerance.

- Smart investors buy to rent — unlocking tax benefits and passive income from day one, even with 100% financing.

- The smartest buyers don’t just chase square meters — they make financially sound, tax-optimized, and long-term decisions.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe Big Financial Question: Can You Really Afford That Property?

If you earn the average German salary of €50,000, can you afford a mansion in Munich or just a fixer-upper in the countryside? It’s a question that matters more than you think. Overbuying is one of the biggest financial mistakes you can make — and one that can impact your future for decades. But don’t worry. In this article, we’ll walk you through exactly how banks determine your borrowing capacity, and more importantly, how you can use smarter calculations to assess what you can truly afford.

We’ll break down essential factors like net income, down payments, interest rates, and even real-life examples so you can compare yourself. Whether you’re dreaming of owning your home or considering investing in property to rent out, this guide will help you avoid common traps and make an informed decision. Let’s dive in and find out what your salary can really buy in today’s German property market.

Why Your Net Salary Shapes Your Budget

The first big factor that determines how much home you can afford is your net salary — that’s your income after taxes, health insurance, and public pension deductions. From this number, financial planners often apply the 50-30-20 rule. This means 50% of your net salary should cover essential needs (like rent or mortgage), 30% for wants (like entertainment), and 20% for savings and investments. But where does your future home fit in? Is it a “need” or an “investment”?

While some treat home ownership as an investment, it’s better seen as a necessary expense — especially since your own home doesn’t generate income. You’re not earning from it; you’re spending on it. In fact, the interest you pay on your mortgage is just as “wasted” as rent — but it doesn’t feel that way emotionally. That’s why many financial experts suggest renting where you live and buying to rent out. This offers tax benefits and passive income — a smarter path if you truly want to invest in property.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationDon’t Forget the Down Payment and Closing Costs

Before thinking about how big a mortgage you can take on, you need to calculate how much cash you can put down. In Germany, closing costs—including property transfer tax, notary fees, and possible agent commissions—typically add up to 10% of the property’s value. And here’s the kicker: banks usually don’t finance these closing costs. You’ll need to bring that in cash.

Then there’s the down payment, often another 10% of the purchase price. Combined, that means you’ll likely need 20% of the property price upfront. That’s a lot of money to save.

However, there are exceptions. Some banks offer 100% financing if you have a strong financial profile and the property is considered low risk. But this means higher monthly payments and significantly more interest paid over time. You’ll also need a stellar credit score and stable income. So before signing anything, check how much you’ve saved — and be realistic about what that can buy you.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationWhy Interest Rates Can Make or Break Your Purchase

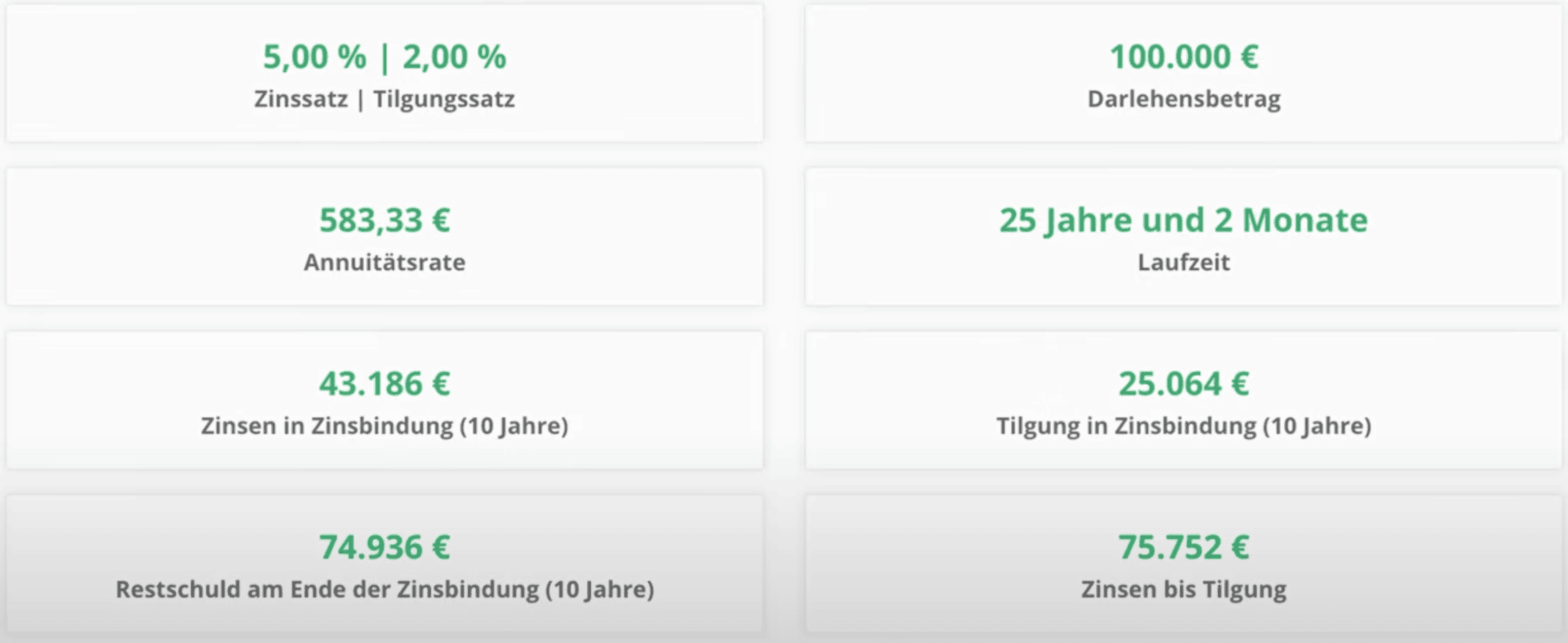

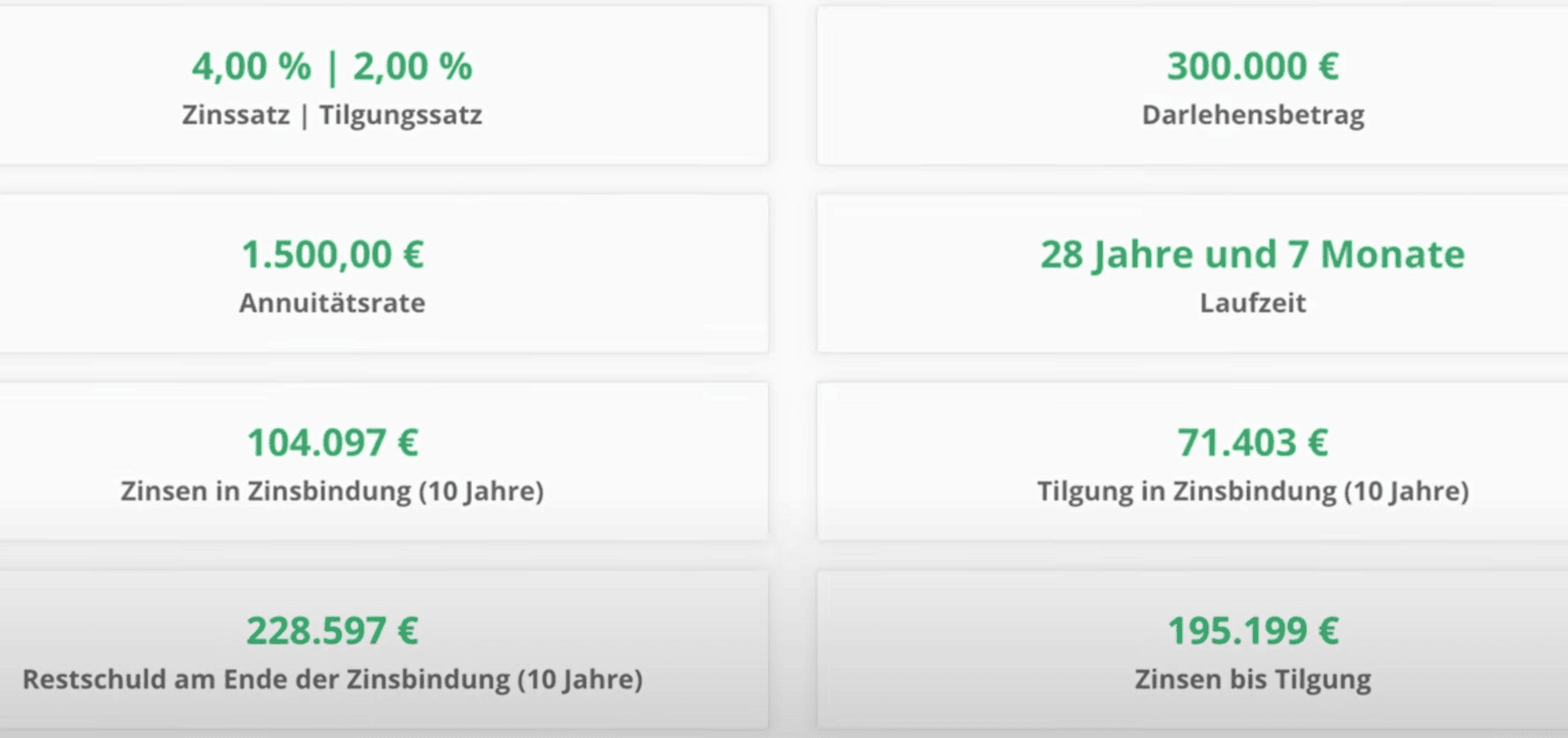

Interest rates are often overlooked when dreaming about home ownership — but they might be the single most important financial factor. Let’s break it down. If you borrow €100,000 at 4% interest with a 2% repayment rate, your monthly payment will be about €500. Over time, that adds up to €65,000 in interest payments — none of which are tax-deductible unless you rent the property out.

Now let’s say interest rates increase to 5%. That bumps your monthly payment to around €583 — a 17% increase. And over the life of your mortgage? That’s €75,000 in interest instead of €65,000. This example shows how sensitive real estate affordability is to interest rates. That’s why it’s essential to shop around for mortgage offers. Our team compares rates from over 800 banks in Germany to help buyers like you find the lowest possible rate — potentially saving you thousands.

Example 1: Single Buyer on an Average Salary

Let’s walk through a real-life example. A 30-year-old single buyer earns €3,000 net per month and has saved up €20,000. He wants to stop renting and buy a starter flat. To keep costs manageable, he goes with a 1.5% repayment rate — allowed because he’s still young.

Using the 50-30-20 rule, he could safely allocate up to €1,500/month to needs like housing. Ideally, though, his mortgage shouldn’t exceed €1,000/month. With a 4% interest rate and 1.5% repayment, that would qualify him for a mortgage of around €220,000. Add his €20,000 savings, and he’s looking at homes priced between €200,000 and €220,000 — assuming 100% financing and minimal closing costs (like in Bavaria).

In large cities like Munich, this won’t get him far. But in smaller towns or rural areas, it could be enough to buy a modest flat. This example shows how savings and regional prices drastically affect affordability.

Example 2: Dual Income Couple with Children

Now let’s consider a couple in their 40s, earning a combined €5,000/month and having saved €80,000. Their goal is to buy a home in a suburban area to raise kids. At their age, banks expect a minimum 2% repayment — higher than for younger buyers. Using a €1,500/month mortgage budget, they could afford a property worth €300,000 with no down payment — or €350,000 if they use all their savings.

But if they’re willing to stretch their budget to €2,000/month — 40% of their income — they could afford up to €440,000. Their bigger income and capital offer more flexibility, but also raise the stakes. One wrong financial move could have long-term consequences. That’s why proper planning — and professional mortgage comparison — are critical at this stage.

Example 3: Buying to Rent Instead of Living In

Here’s the smarter route — buying investment property instead of living in the home. Let’s say you have the same €3,000/month income and €20,000 in savings as our first example. Instead of buying an overpriced city flat, you purchase a small rental property in a B-location like a Düsseldorf suburb.

With €25,000 in closing costs, the rest is 100% financed. Because it’s a new building, you benefit from tax-deductible depreciation. That’s how your property can become cash flow positive from day one. Or take a renovation project in Augsburg. Thanks to low closing costs in Bavaria, you only need €15,000 upfront. And the renovation costs? Mostly tax-deductible — meaning you can recoup much of your investment within a year.

These are the kinds of strategies professionals use. Instead of locking your capital into a home you live in, you can generate income and benefit from major tax breaks.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationConclusion

Whether you’re buying a home to live in or looking for your first investment property, understanding how salary, savings, interest rates, and strategy work together is critical. Don’t let emotions or online myths guide your biggest financial decision.

Think like an investor, compare offers, and plan your next move wisely. Want help figuring out what you can actually afford? Book a free meeting with our team and get expert guidance based on your personal finances.

Pingback: Fix & Flip of a Messy Flat in Germany